Abstract

This study aims to systematically examine the relationship between governance and Islamic banking performance from theoretical, empirical, and strategic perspectives. A Systematic Literature Review (SLR) was conducted on 43 selected articles published between 2016 and 2025 indexed in Scopus, DOAJ, and Google Scholar. The findings indicate that Islamic banking governance has evolved into a multidimensional framework integrating agency theory, stakeholder theory, legitimacy theory, and stewardship theory within a maqashid-based sharia governance structure. Empirical evidence demonstrates that governance mechanisms significantly influence profitability, efficiency, and risk stability, although the strength of these relationships is context-dependent and shaped by regulatory environments and implementation quality. Strategically, governance functions as a competitive instrument that enhances long-term sustainability. This study proposes an integrated conceptual framework to strengthen governance development and managerial practices in Islamic banking.

Keywords

Corporate Governance; Sharia Governance; Islamic Bank Performance; Strategic Sustainability.

Introduction

The development of the global and national Islamic banking industry has shown significant growth in terms of assets, branch networks, and the number of customers over the past two decades, making it an important part of the national financial system in many Muslim countries [1]. This growth has not only resulted in an expansion in institutional size but has also increased the complexity of institutional governance, which must be able to integrate Sharia principles with modern management and governance practices, including compliance with the principles of good corporate governance (GCG) and sharia governance [2]. Consequently, governance has become a strategic element that not only affects the credibility and sustainability of institutions but also influences stakeholders’ trust in the Islamic banking system as a whole [3]. Moreover, Islamic banking institutions in Indonesia, such as Bank Syariah Indonesia, face increasing demands to maintain a balance between Sharia compliance, operational efficiency, and competitive financial performance amid growing competition with conventional banking systems, thereby reinforcing the relevance of studies on governance and performance in Islamic banks [4]. Therefore, a deeper understanding of the relationship between governance frameworks and performance becomes essential to be examined comprehensively within the context of this dynamic industry development.

Conceptually, Islamic banking governance encompasses a broader framework than conventional corporate governance because it emphasizes the integration of Sharia principles through sharia governance, which aims to ensure that all banking operations comply with Islamic laws and values [5]. Previous literature indicates that governance quality has significant implications for institutional performance, where variables such as the size of the Sharia Supervisory Board (SSB), audit committees, and the structure of the board of commissioners are often associated with financial performance indicators such as Return on Assets (ROA) and Return on Equity (ROE) [6]. However, empirical findings remain relatively diverse. Some studies report a positive effect of governance on performance [7], while others reveal insignificant or even contradictory relationships between governance dimensions and performance outcomes [8]. These differences are partly influenced by variations in regulatory contexts and institutional characteristics across countries, as well as the performance measurement approaches employed. This situation opens opportunities for broader discussion through strategic literature studies on governance and performance in Islamic banking in the future.

A number of studies over the past decade have examined the relationship between governance and Islamic banking performance using various empirical approaches, yet their findings remain inconclusive. A study by Mollah et al. [9] shows that sharia governance mechanisms, particularly the effectiveness of the Sharia Supervisory Board (SSB), play a significant role in enhancing the stability and firm value of Islamic banks, although their impact on short-term profitability tends to be contextual. Furthermore, Touti [10] found that the characteristics of the SSB, including the size and expertise of its members, positively influence financial performance (ROA and ROE) with statistical significance at the 5% level. In a more recent context, an integrative study by Nisa et al. [11] on the role of the Sharia Supervisory Board confirms that the effectiveness of Sharia oversight mechanisms not only affects compliance aspects but also contributes to strengthening legitimacy and sustaining the performance of Islamic banks. In addition, a cross-country comparative study by Febryana and Hidayanti [12] demonstrates that the quality of sharia governance has a positive relationship with the social performance of Islamic banks, expanding performance indicators beyond financial dimensions to include social aspects. These findings indicate that the literature has evolved in a multidimensional manner; however, it still shows fragmentation in variables and methodological approaches, thus failing to form a comprehensive conceptual synthesis.

Research in Asia and the Middle East suggests that institutional characteristics and the quality of domestic governance also influence the relationship between governance and performance. Alam et al. [13] found that internal governance quality significantly affects cost efficiency and risk stability in Islamic banks using the Data Envelopment Analysis (DEA) approach. Empirical studies in Indonesia by Mulyany and Hidayat (2018) reveal that the effectiveness of audit committees and Sharia supervision significantly affects Non-Performing Financing (NPF) with a significance level below 5%. Nevertheless, several recent studies such as Khamar [14] report that variables such as CEO duality and ownership concentration do not always have a significant effect on ROA and ROE, resulting in empirical inconsistencies. Furthermore, Hidayanti [11], in a study on governance and digital transformation in Islamic banking, emphasizes that modern governance also encompasses system interoperability, data protection, and Sharia compliance in the digital era. Research by Hasibuan and Soemitra [15] on non-bank Islamic financial institutions also shows that strengthening institutional governance contributes to expanding financial inclusion and systemic stability, which indirectly affects the performance of the Islamic financial industry. Overall, empirical approaches—including panel regression, DEA, and integrative literature review—still produce diverse conclusions, highlighting the urgency of a systematic literature synthesis to develop a more integrated understanding of governance and performance in Islamic banking.

The fragmentation of empirical findings and the diversity of methodological approaches in the literature on governance and Islamic banking performance indicate an urgent need to integrate knowledge systematically. Differences in regulatory contexts, cross-country sample sizes, variations in performance indicators such as ROA, ROE, Cost to Income Ratio, and risk stability—as well as differences in the operational definitions of governance variables—make research findings difficult to compare directly. In addition, most studies still focus primarily on the structural dimensions of governance, while strategic aspects and long-term institutional dynamics have not yet been comprehensively mapped. In this context, a systematic literature synthesis approach becomes crucial to identify consistent patterns of relationships, evaluate the strength of empirical evidence, and map existing research gaps. By integrating theoretical perspectives, including agency theory, stakeholder theory, and the sharia governance framework, with empirical findings across jurisdictions, this study seeks to develop a more robust understanding of how governance influences the performance of Islamic banking from a strategic perspective. Based on this background, this study aims to systematically examine the development of literature on the relationship between governance and Islamic banking performance from theoretical, empirical, and strategic perspectives. This study is directed at mapping dominant governance models in the literature, identifying patterns of performance findings based on various quantitative indicators, and highlighting inconsistencies and research gaps that require further exploration. Thus, this research is expected to produce an integrated conceptual framework and provide significant academic contributions to the development of governance studies and managerial practices in Islamic banking in the future.

Methods

This study employs a qualitative approach using the Systematic Literature Review (SLR) method to comprehensively analyze the relationship between governance and the performance of Islamic banking from theoretical, empirical, and strategic perspectives. The SLR approach was chosen because it allows the process of identifying, evaluating, and synthesizing literature to be conducted systematically, transparently, and replicably, thereby minimizing researcher subjectivity and enhancing the academic validity of the findings [16]. This method is also relevant for integrating diverse empirical findings into a unified analytical framework and identifying existing research gaps. The data sources were obtained from three reputable academic databases, namely Scopus, DOAJ, and Google Scholar, which include both national and international scholarly articles. The search strategy employed several keywords, including Islamic banking governance, sharia governance, corporate governance in Islamic banking, Islamic bank performance, financial performance, and strategic perspective of Islamic banking. The literature search process followed systematic stages starting from initial identification, screening, and eligibility evaluation of articles, as recommended in systematic literature review protocols. The initial search across all databases produced 34,100 publications. After applying a publication year limitation to the period 2016–2025 to ensure the relevance and novelty of the study, the number of identified articles was reduced to 25,840 publications, of which 8,479 were categorized as review and research articles.

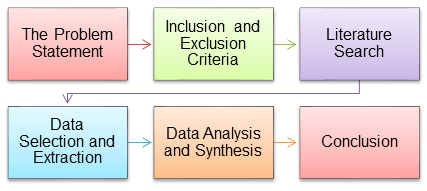

The next stage involved the selection of conceptual review articles and empirical studies relevant to the research focus. The screening process was conducted through an evaluation of titles and abstracts to ensure the substantive relevance to the relationship between governance and Islamic banking performance. Articles that were irrelevant, duplicated, unavailable in full text, or not included in the peer-reviewed category were excluded at this stage. Subsequently, a full-text review was conducted to assess methodological consistency, clarity of governance variables, performance indicators used, and their theoretical and practical contributions. This process aligns with the stepwise selection approach in systematic literature reviews, which emphasizes transparency and accountability in data reduction (Snyder, 2019). Based on this process, 43 articles were deemed eligible for in-depth analysis. Of these, 28 articles were explicitly used in the sub-analysis discussion covering theoretical, empirical, and strategic dimensions, while the remaining 15 articles served as conceptual reinforcement and comparative references. The analysis process was conducted using thematic synthesis techniques by grouping articles based on research focus, methodological approaches, governance variables used, performance indicators measured, and the main research findings. Thematic synthesis enables the integration of findings across studies to generate a more comprehensive conceptual understanding. Through this process, the study identifies trends in dominant governance models, the consistency of empirical results regarding the financial performance of Islamic banks, and strategic implications for the development of sustainable governance practices. All stages were carried out systematically to ensure methodological rigor and to enhance the credibility and replicability of the research. A clearer illustration of this process can be seen in Figure 1.

Figure 1 illustrates the methodological flow of the study in a systematic and sequential manner. The first stage, The Problem Statement, represents the formulation of the research problem, which focuses on how governance influences the performance of Islamic banking from theoretical, empirical, and strategic perspectives. This stage serves as the conceptual foundation that determines the overall direction of the literature review process. The second stage, Inclusion and Exclusion Criteria, describes the process of establishing article selection criteria. At this stage, several parameters were determined, including the publication year range (2016–2025), peer-reviewed scholarly articles, substantive relevance to governance and Islamic banking performance, and the availability of full-text articles. This stage functions to filter the literature so that only high-quality and relevant studies are analyzed further. The third stage, Literature Search, illustrates the process of searching for articles in the Scopus, DOAJ, and Google Scholar databases using predetermined keywords. This stage produced a total of 34,100 publications prior to screening and 25,840 publications after applying the publication year limitation. The fourth stage, Data Selection and Extraction, represents the selection process through screening of titles, abstracts, and full-text reviews from 8,479 articles, resulting in 43 final articles. At this stage, data extraction was also conducted, including the identification of governance variables, performance indicators, research methods, and the main findings of each study. The fifth stage, Data Analysis and Synthesis, describes the thematic analysis of the 43 selected articles, with 28 articles discussed in depth in the sub-analyses. At this stage, the studies were categorized based on theoretical, empirical, and strategic perspectives to identify patterns, consistency of findings, and existing research gaps. The final stage, Conclusion, represents the process of drawing conclusions based on the results of the literature synthesis, providing a comprehensive overview of the relationship between governance and Islamic banking performance as well as its strategic implications.

Result and Discussions

Theoretical Perspective: Conceptualization of Governance in Islamic Banking

The theoretical review indicates that the evolution of the corporate governance concept in Islamic banking does not merely adopt conventional supervisory mechanisms but also expands them through the framework of sharia governance, which emphasizes Sharia compliance and moral accountability. The literature highlights that the governance structure of Islamic banks involves a dual supervisory layer, namely the board of commissioners and the Sharia Supervisory Board (SSB), which function to ensure compliance with Islamic principles and mitigate agency conflicts [9]. Theoretically, this approach integrates agency theory within the context of religious compliance while simultaneously extending it through stakeholder theory, as Islamic banks hold responsibilities not only to shareholders but also to society and the principles of maqasid al-shariah [17]. Comparative studies also show that Islamic banks with active Sharia supervisory boards tend to possess stronger social legitimacy, supporting legitimacy theory within the context of value-based institutions [18]. In addition, stewardship theory explains that Islamic bank management is expected to act as a trustee of entrusted resources rather than merely as rational economic agents [19]. Conceptually, the literature concludes that governance in Islamic banking forms a normative and structural framework that potentially has strategic implications for long-term stability and performance.

The literature defines governance in Islamic banking as a regulatory and supervisory system that is not only oriented toward corporate control mechanisms but is also grounded in Islamic legal principles emphasizing moral integrity, justice, and social responsibility. This concept positions Sharia compliance as a central element in the institutional structure, thereby framing Sharia governance as an extension of conventional corporate governance with a stronger normative dimension. In this context, maqasid al-shariah serves as the institutional objective that directs Islamic banks toward achieving social welfare and equitable economic distribution, which empirically has been associated with improved institutional performance and legitimacy [20]. The role of the Sharia Supervisory Board (SSB) represents the main distinction from conventional governance models, as this institution provides advisory oversight and ensures operational conformity with Sharia principles [21]. Structurally and normatively, Sharia governance emphasizes transparency, accountability, and ethical integrity as organizational foundations [22]. Unlike conventional governance, which primarily focuses on shareholder value maximization and financial indicators, Sharia governance broadens this orientation by incorporating a wider spectrum of stakeholders, including society and communities, as part of the institution’s social responsibility [23]. The dominant theoretical framework explaining the relationship between governance and performance in Islamic banks tends to emphasize an Islamic governance model that integrates ethical and moral dimensions into performance evaluation, in contrast to conventional approaches that focus primarily on financial ratios. Nevertheless, several studies also highlight that despite its strong normative framework, challenges related to compliance and supervisory effectiveness remain issues requiring stronger implementation mechanisms [24].

Interpretatively, both discussions demonstrate consistency in viewing governance in Islamic banking as a hybrid theoretical construct that integrates modern corporate governance mechanisms with normative principles rooted in Sharia. The literature reveals the dominance of a multi-theoretical framework, where agency theory explains the need for monitoring mechanisms to reduce agency conflicts, stakeholder theory broadens the institutional responsibility orientation, legitimacy theory emphasizes the importance of value-based social acceptance, and stewardship theory positions management as moral custodians. Evaluation of these findings indicates that the primary difference between conventional and Islamic governance lies not only in institutional structures such as the presence of the Sharia Supervisory Board but also in their purpose orientation and epistemological foundations. While conventional governance originates from economic rationality and market efficiency, Islamic governance is rooted in the integration of ethical values, maqasid al-shariah, and social responsibility. However, the literature also indicates a gap between the normative framework and practical implementation, particularly in terms of supervisory effectiveness and consistency of Sharia compliance. Thus, Sharia governance can be understood as a normative–structural model that is conceptually robust but still faces challenges in operationalization and cross-jurisdictional standardization.

Empirical Perspective: The Influence of Governance on Islamic Banking Performance

Empirical studies indicate that governance variables have diverse relationships with the performance of Islamic banking institutions. A cross-country study by Nomran dan Haron [25] found that the size of the Sharia Supervisory Board has a significant positive effect on Return on Assets (ROA) with a regression coefficient of 0.12 at the 5% significance level. Research by Mollah et al. [9], involving 52 Islamic banks in 14 countries, shows that board independence and dual Sharia oversight structures contribute to an average increase in ROE of approximately 1.8% compared to banks lacking strong supervisory structures. Meanwhile, Bukair and Rahman [26], updated in post-2016 follow-up studies, indicate that concentrated ownership structures may improve operational efficiency but do not always significantly affect the Capital Adequacy Ratio (CAR). Grassa [27] found that board meeting frequency positively correlates with profitability, although the effect weakens in smaller banks. Conversely, research by Farag et al. [28]suggests that in some national contexts, the influence of governance on performance is not statistically significant due to differences in regulatory and institutional environments. Overall, empirical synthesis reveals a dominant pattern of positive relationships between governance and performance, although consistency varies depending on geographical context and bank size.

Recent empirical studies further reinforce the finding that governance significantly affects the financial performance of Islamic banks, although the level of consistency varies across variables and national contexts. Indicators of Good Corporate Governance (GCG) have generally been shown to positively influence profitability and efficiency, where more comprehensive GCG implementation correlates with higher ROA and ROE ratios in Indonesian Islamic banks [29]. In terms of Sharia governance, the presence and effectiveness of Sharia supervisory mechanisms demonstrate positive relationships with financial performance, particularly in profitability and stability indicators such as ROA and non-performing financing ratios [30]. Variables such as board size and independence are among the most frequently tested determinants, with findings suggesting that larger boards and a higher proportion of independent commissioners are associated with improved financial performance and stronger monitoring functions [31]. However, the effectiveness of internal auditing presents more complex results; although theoretically strengthening internal control systems, several studies have found negative relationships with profitability when audit functions are not implemented efficiently. Cross-regional studies also demonstrate substantial variability in results. Research conducted in the Middle East and Southeast Asia indicates that the effect of governance on performance is influenced by regulatory quality and the maturity level of the Islamic financial industry. Additionally, variations in observation periods influence the consistency of results because regulatory changes, macroeconomic conditions, and market dynamics may moderate the governance–performance relationship [32]; [33]. Consequently, although most studies demonstrate a positive relationship between governance and Islamic bank performance, empirical literature emphasizes that this relationship is contextual and influenced by institutional and temporal factors.

From an evaluative perspective, both discussions indicate that empirical evidence tends to support the hypothesis of a positive relationship between governance and Islamic banking performance, particularly regarding profitability indicators such as ROA and ROE. The variables most consistently demonstrating significant effects include board size and independence, the presence and effectiveness of the Sharia Supervisory Board, and the quality of Good Corporate Governance implementation. However, the strength of this relationship is not universal. Moderate regression coefficients—such as an average ROE increase of 1–2% or effect coefficients around 0.10–0.15—suggest that governance is an important factor but not the sole determinant of performance. Moreover, inconsistent findings related to ownership structure, board meeting frequency, and internal auditing suggest potential moderating effects from bank size, regulatory quality, and institutional environments. In other words, governance functions as an enabling mechanism, whose effectiveness strongly depends on structural and geographical contexts. This implies that cross-country generalization of findings must be approached cautiously and requires comparative and longitudinal approaches to better understand the dynamics of the governance–performance relationship.

Strategic Perspective: Governance Implications for Sustainability and Competitiveness of Islamic Banks

Strategic literature indicates that governance serves both as a risk mitigation instrument and a driver of long-term competitiveness. Research by Alam et al. [34] found that Islamic banks with higher governance index scores exhibit lower Non-Performing Financing (NPF) ratios by an average of 0.9% compared to banks with lower governance scores. Fatmawati [35] emphasizes that Sharia supervisory mechanisms enhance stakeholder trust and strengthen institutional reputation, indirectly contributing to increased third-party funds. Furthermore, Safiullah dan Shamsuddin [36] demonstrate that strong governance structures contribute to stability during crisis periods, with lower profit volatility compared to conventional banks. In the context of sustainability, Lestari [37] highlights the integration of Environmental, Social, and Governance (ESG) principles within Sharia frameworks as a competitive differentiation strategy. A recent study by Fakhira [38] in Indonesia shows that implementing governance based on Sharia compliance contributes to strengthening social legitimacy and operational sustainability of Islamic banks. Overall, these findings confirm that governance is not merely a control mechanism but a strategic instrument that enhances stability, reputation, and competitiveness in the Islamic banking industry.

Recent strategic studies further emphasize that Sharia governance has direct implications for the long-term sustainability of Islamic banks through strengthening economic, social, and environmental dimensions. The Sharia Supervisory Board (SSB) plays a key role in ensuring Sharia compliance while simultaneously encouraging sustainability performance. Puspitasari and Kasri [39] found that the frequency of SSB meetings and the competence of its members positively correlate with improvements in the social and environmental performance of Islamic banks. Similar findings were reported by Toumi dan Hussainey [40], who demonstrated that effective Sharia governance enhances ESG scores and strengthens institutional competitiveness in global financial markets. From a maqasid al-shariah perspective, governance implementation aligned with Islamic legal objectives improves service quality and firm value, thereby contributing to long-term sustainability [20]. In terms of crisis resilience, a strong governance framework enables Islamic banks to maintain operational stability and market trust during periods of economic uncertainty [41]. Additionally, effective governance has been shown to build reputation and public trust, which constitute important social capital in strengthening customer loyalty and competitive positioning within the industry [42]. Nevertheless, several studies highlight implementation challenges, including the lack of standardized governance practices and potential supervisory failures, which may hinder the optimal achievement of sustainability goals. Consequently, Sharia governance is positioned as a strategic foundation determining resilience, reputation, and sustainability in the Islamic banking industry.

From an evaluative standpoint, both discussions indicate that governance in Islamic banking has evolved from merely an internal control mechanism into a strategic instrument influencing stability, reputation, and long-term competitiveness. Empirical evidence showing a reduction in NPF ratios by approximately 0.9% among banks with high governance scores, as well as lower profit volatility during crisis periods, indicates that governance functions as a tangible risk mitigation mechanism. On the other hand, improvements in ESG scores and strengthened social legitimacy demonstrate that Sharia governance contributes to sustainable value creation. A comprehensive interpretation of the literature suggests that the competitive advantage of Islamic banks is determined not only by Sharia-based product differentiation but also by the credibility of their governance systems. However, the strategic effectiveness of governance strongly depends on the quality of implementation, the competence of the Sharia Supervisory Board, and regulatory consistency. Challenges such as the absence of cross-jurisdictional governance standardization and the risk of ceremonial compliance may weaken governance’s strategic impact if not accompanied by stronger institutional capacity building. Therefore, Sharia governance should be understood as a strategic capability requiring integration between formal structures, organizational culture, and managerial ethical commitment.

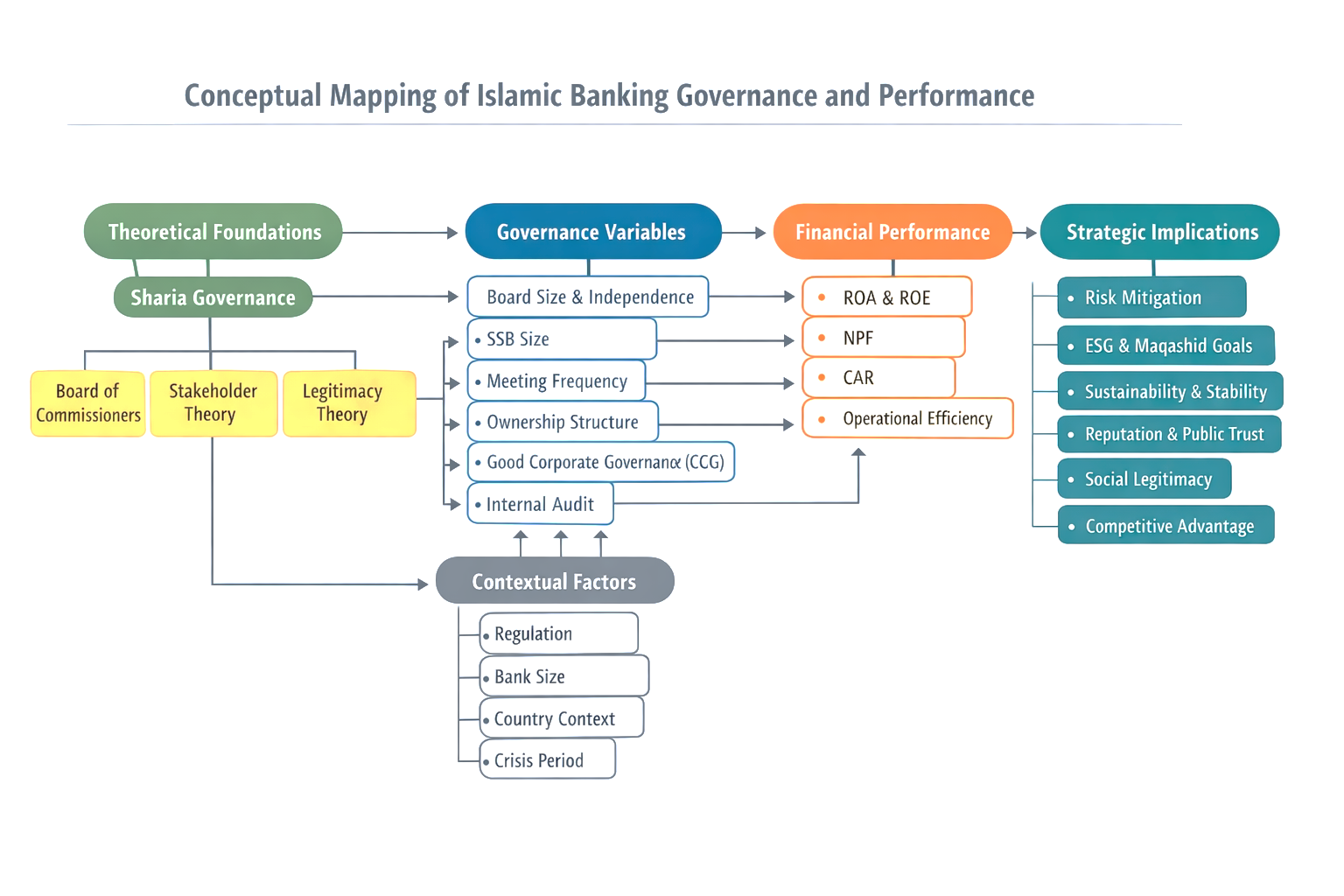

Based on the synthesis of research findings presented across three main perspectives—theoretical, empirical, and strategic—a number of key concepts and central variables shaping the development of governance research in Islamic banking can be identified. To facilitate the visualization of relationships among variables and to clarify the conceptual flow from governance structures to their strategic implications, a conceptual mapping is presented in the form of a mind map. This mapping aims to illustrate the interconnections between the fundamental concepts of sharia governance, the empirical variables tested in previous studies, and their strategic implications for the sustainability and competitiveness of Islamic banks, as summarized in Figure 2.

Figure 2 illustrates the evolving structure of research on governance in Islamic banking in a gradual and integrated manner. From the conceptual perspective, governance is understood through the framework of sharia governance, which emphasizes sharia compliance, a dual governance system, and theoretical foundations such as agency theory, stakeholder theory, legitimacy theory, and stewardship theory. The supervisory structure involving the board of commissioners and the Sharia Supervisory Board (SSB) serves as the normative and institutional foundation that distinguishes this model from conventional governance systems. At the empirical level, research primarily focuses on testing governance variables such as board size and independence, SSB size, meeting frequency, ownership structure, Good Corporate Governance (GCG), and internal audit, which are then linked to financial performance indicators including Return on Assets (ROA), Return on Equity (ROE), Non-Performing Financing (NPF), Capital Adequacy Ratio (CAR), and operational efficiency. However, these relationships are not universal; they are influenced by contextual factors such as regulatory frameworks, bank size, country context, and crisis periods. From a strategic perspective, governance is positioned as an instrument for risk mitigation, strengthening institutional stability, and promoting sustainability through the integration of Environmental, Social, and Governance (ESG) principles and maqashid-based performance frameworks. Furthermore, effective governance contributes to institutional reputation, public trust, social legitimacy, and competitive advantage. Interpretatively, this mind map indicates that the development of research has progressed from a normative–structural understanding toward empirical verification, and ultimately toward strategic implications. This progression confirms that sharia governance represents a multidimensional determinant influencing the performance, stability, and long-term competitiveness of the Islamic banking industry.

Based on the integration of theoretical, empirical, and strategic perspectives, the findings of this study demonstrate that governance in Islamic banking has evolved into a multidimensional framework that integrates formal institutional structures, normative Islamic values, and long-term sustainability orientations. Theoretically, the literature positions sharia governance as an integrative model that extends conventional corporate governance through the combination of agency theory, stakeholder theory, legitimacy theory, and stewardship theory, with maqashid al-shariah serving as its normative foundation. This conceptualization emphasizes that governance functions not merely as a supervisory mechanism but also as a value-based system that shapes institutional direction and strategic objectives. Empirically, the synthesis indicates that governance exerts a significant influence on Islamic banking performance, particularly in terms of profitability indicators (ROA and ROE), efficiency (Cost-to-Income Ratio), and risk stability. Nevertheless, the strength and consistency of these relationships are context-dependent, influenced by variations in regulatory environments, ownership structures, bank size, and the quality of implementation of the Sharia Supervisory Board and internal control mechanisms. Cross-country findings reveal considerable heterogeneity, suggesting that governance effectiveness is not universal but rather depends on institutional dynamics and the broader industry environment. At the strategic level, the literature leads to the conclusion that sharia governance functions as an instrument for achieving competitiveness and long-term sustainability. The integration of sharia compliance, risk management, and ESG principles strengthens institutional legitimacy, enhances public trust, and supports long-term stability. Consequently, this synthesis emphasizes that the relationship between governance and Islamic banking performance is not merely structural or mechanistic but rather a strategic relationship shaped by the interaction of values, supervisory mechanisms, and institutional contexts. Overall, this study successfully maps the dominant governance models, identifies patterns of influence on various performance indicators, and highlights inconsistencies and research gaps that remain—particularly in the strategic dimension and long-term institutional dynamics. These findings reinforce the urgency of developing an integrated conceptual framework capable of explaining more comprehensively how governance influences Islamic banking performance across different jurisdictions and stages of industry development.

Conclusion

This study originates from the fragmentation of empirical findings and the diversity of methodological approaches in the literature on governance and the performance of Islamic banking, which has made it difficult to establish a robust conceptual generalization. Through a **Systematic Literature Review (SLR)** approach, this study integrates theoretical, empirical, and strategic perspectives to provide a more comprehensive understanding of how governance influences the performance of Islamic banking institutions. From a theoretical perspective, the findings confirm that Islamic banking governance represents a multidimensional construct that extends beyond the framework of conventional corporate governance. The integration of agency theory, stakeholder theory, legitimacy theory, and stewardship theory within the framework of sharia governance indicates that governance functions not only as a control mechanism but also as a value-based system grounded in maqashid sharia, shaping the institutional orientation and social legitimacy of Islamic banks. Empirically, the synthesis demonstrates that governance has a significant influence on key performance indicators, including profitability, efficiency, and risk stability; however, this relationship is not uniform, as variations in regulatory environments, institutional characteristics, bank size, and the quality of sharia supervisory implementation generate heterogeneous findings. These variations indicate that the effectiveness of governance is contextual and depends more on the depth of its implementation than merely on its structural design. At the strategic level, this study identifies that sharia governance functions as an important instrument for building competitiveness and long-term sustainability through the integration of sharia compliance, risk management, and sustainability orientation, which strengthens institutional stability and enhances public trust. Consequently, governance should not be viewed merely as a regulatory obligation but rather as a strategic foundation for the development of the Islamic banking industry. Overall, this study contributes academically by proposing an integrated conceptual framework that maps dominant governance models, identifies patterns of relationships with various performance indicators, and highlights existing research gaps—particularly regarding institutional dynamics and long-term implications—thereby opening opportunities for future studies using comparative, longitudinal, and institutional approaches to further strengthen the theoretical and practical foundations of Islamic banking governance.

References

- Hisam Muhammad TINJAUAN KINERJA BANK SYARIAH INDONESIA (BSI): PERKUAT ASET DAN VISI MISI YANG EFEKTIF Currency (Jurnal Ekonomi Dan Perbankan Syariah) 02 DOI ↗ Google Scholar ↗

- Addinda Nur, Sari Iva Kurnia, Sutrisno Hongki LITERATURE REVIEW : ANALISIS PENGARUH INTELLECTUAL CAPITAL DAN ISLAMIC CORPORATE GOVERNANCE TERHADAP KINERJA PERUSAHAAN PERBANKAN SYARIAH DI INDONESIA Journal of Islamic Economics and Finance 1(1) DOI ↗ Google Scholar ↗

- Setyawan Aris, Mukhlisin Murniati, Pramono Eko Pengaruh Kualitas Corporate Governance terhadap kinerja Perbankan Syariah : Studi negara Asia Tenggara Indonesian Journal of Islamic Economics and Business 9(1) DOI ↗ Google Scholar ↗

- Erni Erni, Rehani Najmi, Ilham Ilham Tata Kelola Perbankan Syariah Jurnal Bisnis, Ekonomi Syariah, dan Pajak (JBEP) 2(2) DOI ↗ Google Scholar ↗

- Rama Ali, Novela Yella SHARIAH GOVERNANCE DAN KUALITAS TATA KELOLA PERBANKAN SYARIAH Signifikan: Jurnal Ilmu Ekonomi 4(2) DOI ↗ Google Scholar ↗

- Umiyati U, Maisyarah L, Kamal M Islamic Corporate Governance And Sharia Compliance On Financial Performance Sharia Bank In Indonesia Al-Iqtishad: Jurnal Ilmu Ekonomi Syariah. 12(1) DOI ↗ Google Scholar ↗

- Soveinia Soveinia, Haryanto Hery The Influence of Corporate Governance on the Performance of Islamic Banking Companies in Indonesia Jurnal Ilmiah Ekonomi Islam 8(03) DOI ↗ Google Scholar ↗

- Diana Nur, Syafi Imam, Maulidiyah Nailin Nikmatul GOOD CORPORATE GOVERNANCE TOWARD FINANCIAL PERFORMANCE OF ISLAMIC BANK IN INDONESIA JPS (Jurnal Perbankan Syariah) 5(1) DOI ↗ Google Scholar ↗

- Mollah Sabur, Hassan M Kabir, Farooque Omar, Mobarek Asma The governance, risk-taking, and performance of Islamic banks Journal of Financial Services Research 51(2) DOI ↗ Google Scholar ↗

- Touti Nihal RESEARCH STATUS AND PROSPECTS OF SHARIAH COMPLIANCE IMPACT ON FIRM RISK , PERFORMANCE AND RESILIENCE Journal of Islamic Monetary Economics and Finance 10(4) DOI ↗ Google Scholar ↗

- Nisa J, Aryanti R. S., Hidayanti N. F. Perbankan Terbuka dan Inklusi Keuangan Islam: Memetakan Literatur tentang Interoperabilitas, Privasi, dan Kepatuhan SYIRKAH: Jurnal Ekonomi Syariah 02(02) 2025 DOI ↗ Google Scholar ↗

- Febryana N, Ramadhan S, Imron I, Hidayanti N. F. PERAN DEWAN PENGAWAS SYARIAH DALAM MENINGKATKAN KINERJA KEUANGAN BANK SYARIAH : SEBUAH KAJIAN SISTEMATIS Journal of Management and Innovation Entrepreneurship (JMIE) 2(4) DOI ↗ Google Scholar ↗

- Alam Md. Kausar, Ab Rahman Suhaimi, Mustafa Hasri, Shah Sabarina, Hossain Md Shariah Governance Framework of Islamic Banks in Bangladesh: Practices, Problems and Recommendations Asian Economic and Financial Review 9(1) DOI ↗ Google Scholar ↗

- Khamar Tazilah Mohd, Majid Muhammad, Awee Azeyan, Keang Adam Corporate Governance Characteristics and Financial Performance: Evidence from Islamic Banks in Malaysia Management and Accounting Review (MAR) 20 DOI ↗ Google Scholar ↗

- Hasibuan Heny Liya, Soemitra Andri Kajian Literatur Peran Mikro Keuangan Syariah BMT Dalam Menggerakkan Keuangan Inklusif 8(02) http://dx. DOI ↗ Google Scholar ↗

- Donthu Naveen, Kumar Satish, Mukherjee Debmalya, Pandey Nitesh, Marc Weng How to conduct a bibliometric analysis : An overview and guidelines Journal of Business Research Elsevier Inc. 133(May) DOI ↗ Google Scholar ↗

- Lestari Irna, Hanafi Mamduh, Wardhana Leo The Evolution of Islamic Corporate Governance from the Early Ages to the Sustainable Development Goals’ (SDGs) Era International Journal of Islamic Finance and Sustainable Development 16(3) DOI ↗ Google Scholar ↗

- Nomran Naji Mansour, Haron Razali, Hassan Rusni Shari’ah supervisory board characteristics effects on Islamic banks’ performance: Evidence from Malaysia International Journal of Bank Marketing 36(2) DOI ↗ Google Scholar ↗

- Almutairi Ali R, Quttainah Majdi Anwar Corporate governance: evidence from Islamic banks Social Responsibility Journal 13(3) DOI ↗ Google Scholar ↗

- Kiranawati Yenik, Aziza Shifa, Nasim Arim, Ningsih Caria Islamic Banking Governance in Maqashid Sharia Perspectives: A Systematic Literature Review Share: Jurnal Ekonomi dan Keuangan Islam 12(1) DOI ↗ Google Scholar ↗

- Zahid Syeda Nitasha, Khan Imran Islamic Corporate Governance: The Significance and Functioning of Shari’ah Supervisory Board in Islamic Banking Turkish Journal of Islamic Economics (TUJISE) 6(1) DOI ↗ Google Scholar ↗

- Nofianti Leny, Irfan Andi, Zakaria Nor Balkish Islamic Governance for Managing Banking Performance Assessment Asia-Pacific Management Accounting Journal 17(3) DOI ↗ Google Scholar ↗

- Hamid Ahmad Munir ISLAMIC GOVERNANCE IN ISLAMIC SCHOOL FINANCE Cendekia: Jurnal Pendidikan dan Pembelajaran 12(1) DOI ↗ Google Scholar ↗

- Khan M. Mansoor Islamic Banking and Finance : Shariah Governance in Theory and Practice Journal of Management Research (JMR) 11(2) DOI ↗ Google Scholar ↗

- Nomran Mansour Naji, Haron Razali, Hassan Rusni Bank Performance and Shari ’ ah Supervisory Board Attributes of Islamic banks : Does Bank Size Matter ? Journal of Islamic Finance (JIF) 2117 DOI ↗ Google Scholar ↗

- Bukair Abdullah, Rahman Azhar Bank performance and board of directors attributes by Islamic banks International Journal of Islamic and Middle Eastern Finance and Management 8(3) DOI ↗ Google Scholar ↗

- Grassa Rihab Corporate governance and credit rating in Islamic banks: Does Shariah governance matters? Journal of Management & Governance 19(3) DOI ↗ Google Scholar ↗

- Farag Hisham, Mallin Chris, Ow-Yong Kean Corporate Governance in Islamic Banks: New Insights for Dual Board Structure and Agency Relationships Journal of International Financial Markets, Institutions and Money 54 DOI ↗ Google Scholar ↗

- Jaziroh W, Nirwana N. Q. S. Governance and Risk Management in Sharia Banks and Financial Performance Indonesian Journal of Law and Economics Review 19(4) DOI ↗ Google Scholar ↗

- Alarabeyyat Ahmad Abed Alhaleem Ahmad, Kadir Mohd Rizuan Abdul, Kamarudin Khairul Anuar, Sapingi Raedah Bte., Al-Dalaien Ahmad Balancing Faith and Finance : How Ownership Structures Shape the Impact of Shariah Governance on Islamic Bank Performance WSEAS transactions on systems 24 DOI ↗ Google Scholar ↗

- Akhyar Ahmad Musthafainal, Hussin Nazimah Governance Structures as Drivers of Performance in Islamic Banks International Journal of Academic Research in Business and Social Sciences 15(9) 2025 DOI ↗ Google Scholar ↗

- Kurniawan Ferdian Ari, Hanggraeni Dewi Risk Governance Unlocks Islamic Banks ’ Dual Performance Goals JBMP (Jurnal Bisnis, Manajemen & Perbankan) 10(2) DOI ↗ Google Scholar ↗

- Aslam Ejaz, Haron Razali Corporate governance and risk-taking of Islamic banks: evidence from OIC countries Corporate Governance 21(7) DOI ↗ Google Scholar ↗

- Rashid Abdul, Akmal Muhammad, Shah Syed Muhammad Abdul Rehman Corporate governance and risk management in Islamic and convectional financial institutions: explaining the role of institutional quality Journal of Islamic Accounting and Business Research 15(3) DOI ↗ Google Scholar ↗

- Fatmawati Dewi, Mohd Ariffin Noraini, Zainal Abidin Nor Hafizah, Osman Ahmad Shari'ah governance in Islamic banks: Practices, practitioners and praxis Global Finance Journal 51 DOI ↗ Google Scholar ↗

- Safiullah Md, Shamsuddin Abul Risk in Islamic banking and corporate governance Pacific-Basin Finance Journal 47 DOI ↗ Google Scholar ↗

- Lestari Irna Puji, Hanafi Mamduh Mahmadah, Wardhana Leo Indra SUSTAINABILITY-BASED ISLAMIC CORPORATE GOVERNANCE AND ISLAMIC BANKS ’ MULTI- PERFORMANCE : EVIDENCE FROM INDONESIA Journal of Islamic Monetary Economics and Finance 11(4) 2025 DOI ↗ Google Scholar ↗

- Fakhira Dhia, Utami Meisyah, Wulandari Afifah, Aryanti Aryanti Peran Bank Syariah dalam Mendukung Ekonomi Berkelanjutan SJEE (Scientific Journals of Economic Education) 9(2) DOI ↗ Google Scholar ↗

- Puspitasari Novia Dwi, Kasri Rahmatina Awaliah Shariah board governance and sustainability performance : analysis of sharia banking in Indonesia Jurnal Ekonomi & Studi Pembangunan 24(2) DOI ↗ Google Scholar ↗

- Boudawara Yossra, Toumi Kaouther, Wannes Amira, Hussainey Khaled Shari'ah governance quality and environmental, social and governance performance in Islamic banks. A cross-country evidence Journal of Applied Accounting Research 24(5) DOI ↗ Google Scholar ↗

- Suryono Agus Budi TATA KELOLA PERBANKAN SYARIAH YANG BERKELANJUTAN: ANALISIS TERHADAP KESATBILAN EKONOMI BERDASARKAN PRINSIP SYARIAH (Menelusuri Dampak Positif Tata Kelola Perbankan Syariah terhadap Stabilitas Ekonomi Global dan Penerapannya) Jurnal Al Wadiah DOI ↗ Google Scholar ↗

- Norchaeva Sabrina Norchaevna Islamic Finance : Principles , Governance , Sustainability and Investment Insights European Journal of Management, Economics and Business 1(3) DOI ↗ Google Scholar ↗