Abstract

This study examines the relationship between ownership structure and opportunistic real activity manipulation in non-financial firms listed on the Nairobi Securities Exchange. The analysis is grounded in Agency Theory and utilizes secondary panel data comprising 416 firm-year observations covering the period 2008–2023. The findings reveal that institutional and foreign ownership structures serve as effective corporate governance mechanisms that enhance financial reporting quality through active monitoring of managerial opportunistic behavior. By strengthening oversight and participation in corporate decision-making, these ownership structures mitigate agency conflicts and align managers’ interests with those of shareholders. The results further suggest that stronger ownership monitoring discourages opportunistic real activity manipulation practices. Based on these findings, the study recommends policy reforms aimed at strengthening disclosure requirements, enforcing transparent financial reporting, and improving oversight of ownership structures to curb opportunistic earnings manipulation. In addition, policies that promote investor protection, enhance transparency regarding institutional investor influence, and encourage collective monitoring can improve corporate accountability, attract global investment, and strengthen investor confidence in the market. This study contributes to the growing body of literature on corporate governance and sustainability in emerging economies, particularly within firms listed on the Nairobi Securities Exchange, by highlighting ownership structure attributes as a pivotal factor in promoting transparency and improving financial reporting quality.

Keywords

Opportunistic Real Activity Manipulation (ARAM) Ownership structure Nairobi Securities Exchange

Introduction

Financial reporting is intended to present a faithful representation of a firm’s financial performance and to demonstrate management’s accountability to shareholders. However, according to agency theory, the separation of ownership and control in modern corporations creates potential conflicts of interest and information asymmetry between managers and shareholders. As a result, shareholders rely heavily on reported earnings to assess managerial performance and evaluate the overall financial condition of the firm. Reported earnings are therefore considered important indicators of a company’s value and prospects, guiding decisions related to investment, financing, and operational activities[1]. Nonetheless, the credibility of financial reports has come under increasing scrutiny, as managers may exercise their discretion to influence financial outcomes through earnings management [2] [3]. Earnings management occurs when managers deliberately influence financial reporting to shape stakeholders’ perceptions, potentially leading to decisions based on distorted information [4]. It can take the form of accrual-based strategies, which adjust accounting accruals within standard guidelines to affect reported performance [5] or Opportunistic Real Activity Manipulation (ORAM), which involves operational decisions aimed at influencing earnings [6]. ORAM includes practices such as adjusting credit sales and price reductions to meet short-term targets[7], exceeding normal production to lower per-unit costs despite higher inventory holding costs, and strategically reclassifying or mismanaging operational expenditures to enhance reported income ([3]. Unlike accrual-based methods, ORAM directly affects cash flow and operational efficiency, making it a potent tool for managers to achieve strategic objectives or exercise opportunistic behavior while boosting current-period earnings. The principal–agent conflict underpins Opportunistic Real Activity Manipulation (ORAM), wherein managers exploit operational discretion and engage in unethical or deceptive practices to prioritize managerial benefits over the welfare of shareholders. In pursuing personal or strategic objectives, managers often prioritize short-term reporting goals over shareholder interests, attempting to influence capital markets. For instance, by manipulating stock prices before equity issuances, acquisitions, or share repurchases[8]. Firms may also resort to earnings management to meet analysts’ forecasts [9] or to evade regulatory scrutiny and political pressures. Furthermore, compensation-related incentives—both explicit, such as performance bonuses, and implicit, including professional reputation or job security- reinforce managers’ propensity to engage in opportunistic real activity manipulation, highlighting the persistent tension between managerial opportunism and the maximization of shareholder value[10].

Globally, Opportunistic Real Activity Manipulation has become a pervasive practice in both developed and emerging economies. The PwC Global Economic Crime and Fraud Survey[11] reported that nearly 49% of corporate reports fail to meet expected standards, while high-profile scandals involving Tyco, HealthSouth, Kraft Heinz, and WorldCom [12] highlight their widespread consequences. In Africa, ORAM is also significant. [13] Profile of a Fraudster” Report (2023–2024) found that 37% of reported fraud cases involved manipulation of financial results or accounting records, often by employees seeking to meet performance targets or conceal inefficiencies. Prior literature evidence supports this pattern of widespread opportunistic real activity manipulation within African markets. [14] and Oladipo et al. (2025) further demonstrate extensive engagement in REM among Sub-Saharan listed firms. In Kenya, the Fraud Survey found that 53% of managers believed their companies had over-reported financial performance. Similarly, [15] identified an upward trend in earnings manipulation among Nairobi Securities Exchange-listed firms beginning in 2012, while [16] provided further evidence of REM’s presence among NSE-listed companies, linking it to variations in firm performance. Furthermore, [17] In their study “Nexus Between Real Earnings Management and Company Profitability: An Empirical Analysis of Listed Non-Financial Companies in Sub-Saharan Africa,” they reported significant levels of REM, underscoring its ongoing relevance in corporate financial reporting. These patterns underscore the critical need to examine Opportunistic real activity in the Nairobi Security Exchange, given its implications for financial reporting quality and investor confidence.

Corporate governance is pivotal in restraining opportunistic earnings practices by ensuring managerial actions align with shareholder interests. Ownership structure serves as a key oversight mechanism, aligning executives’ objectives with those of owners and strengthening financial reporting quality [18]. In Kenya, regulatory frameworks such as [19] reinforce the role of ownership in promoting transparent and credible reporting[20]. Yet, despite global governance reforms, earnings manipulation remains pervasive[21]. For instance, Cronos Group in Canada overstated revenue and intangible assets by US$7.6 million and US$234.9 million (2019–2022), while Steinhoff International in South Africa inflated financial statements by approximately €6.5 billion (2017–2025)[22] [23]. Between 2020 and 2021, JATU Plc, a non-financial firm in Tanzania, misappropriated approximately TZS 4–9 billion from investors through fraudulent farm investment schemes with no traceable operations or outputs, exposing serious corporate governance weaknesses[24]. In NSE, non-financial firms continue to face audit queries, reputational damage, operational inefficiencies, and, in extreme cases, delisting. WPP Scangroup suspended its CEO and CFO following 2020 audit irregularities[25] , and Uchumi Supermarket Ltd was suspended in 2021 for failing to comply with reporting obligations [26]. These practices inflict substantial investor losses, depress stock prices, attract regulatory scrutiny, and, in extreme cases, precipitate corporate collapse and market inefficiencies [27].

Literature shows that opportunistic real activity manipulation persists, particularly in emerging economies where weak corporate governance and limited regulatory enforcement facilitate such practices, amplifying their adverse effects[28] . Prior research identifies ownership concentration, managerial opportunism, and governance quality as key determinants of earnings smoothing [29]. However, most ORAM studies have focused on developed economies, including the USA and Europe, leaving a contextual gap in understanding these dynamics in emerging markets[30]. Nairobi Security Exchange offers an ideal setting for such an investigation, as non-financial firms are often controlled by shareholders with significant ownership stakes[31] , a structure that frequently coincides with weaker oversight and greater scope for earnings manipulation [32]. Moreover, a conceptual gap exists; prior studies have predominantly examined ownership structure in relation to accrual-based earnings management[33], with limited focus on its impact on opportunistic real activity manipulation[1] . This study, therefore, seeks to address both the contextual and conceptual gaps by analyzing the association between ownership structure and opportunistic real activity manipulation in non-financial firms listed in Nairobi Securities Exchange.

This study makes several important contributions by examining the association between ownership structure and opportunistic real activity manipulation among publicly listed non-financial firms on the Nairobi Securities Exchange. The findings show that ownership structure significantly influences opportunistic real activity manipulation and offer valuable insights that can inform future research in corporate governance and financial reporting. Practically, the findings guide NSE non-financial firms in developing governance frameworks and best practices to enhance financial disclosure, reduce earnings manipulation, strengthen competitiveness, and attract investment. Investors and shareholders gain guidance on monitoring management, reducing agency conflicts, and aligning owner-manager objectives. Managers can understand how operational decisions and ownership structures affect financial reporting, promoting ethical practices and firm performance. Finally, regulators are informed about governance gaps and reform effectiveness, enabling the enforcement of robust corporate governance standards consistent with international best practices.

This study concentrates on non-financial firms for several key reasons. First, financial institutions, such as banks and insurance companies, operate under strict regulations from authorities like the Central Bank of Kenya and the Insurance Regulatory Authority, which limit access to detailed financial data. They also often employ off-balance-sheet reporting, making it challenging to obtain a clear view of their financial position. Non-financial firms, by contrast, have more discretion over their operational and financial reporting, which makes them more prone to real earnings management. This flexibility makes them ideal for investigating how ownership structure influences earnings practices. Focusing on non-financial firms ensures that the data are both accessible and highly relevant to this study's objectives.

Theoretical Foundation

To underpin the relationships among the study variables, the research draws on a key theoretical framework. Specifically, Agency Theory is applied, as discussed in the following section.

Agency Theory

This study is grounded in Agency Theory (Jensen & Meckling, 1976), which explains the principal-agent relationship between shareholders and managers when ownership is separated from control. Managers may pursue personal interests that conflict with shareholder wealth, creating agency conflicts, often amplified by information asymmetry ([34]. Agency Theory emphasizes that governance mechanisms, particularly ownership structure, can align managerial and shareholder interests. Institutional investors, with expertise and resources, strengthen oversight by influencing strategic decisions, promoting transparency, and participating in board processes[35] [36]. Foreign investors contribute additional monitoring, global knowledge, and access to international capital, further reducing agency conflicts [37][38]. However, ownership structure can also enable opportunistic behavior when investors prioritize short-term gains or face informational constraints, potentially allowing real activity manipulation[39] [40] [41].Agency Theory thus underpins this study by linking ownership structure to managerial opportunism and highlighting the importance of monitoring and accountability.

Conceptual Framework

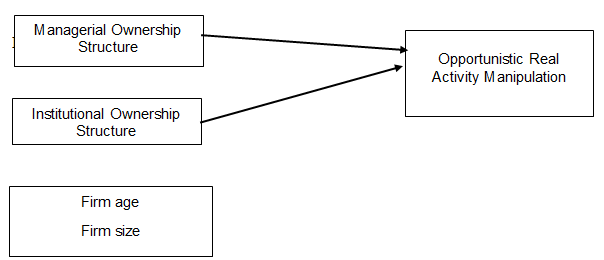

This paper presents a conceptual framework outlining the key variables under investigation. Ownership structure serves as the predictor variable, comprising institutional and foreign ownership, while Opportunistic Real Activity Manipulation represents the outcome variable. The study also controls for firm age and firm size. Institutional ownership brings valuable knowledge and expertise, enabling effective oversight of managerial behavior and reducing agency conflicts ([33] . [42] Further note that institutional investors not only lower the likelihood of artificial earnings but also mitigate the extent of such manipulative practices. Foreign investors contribute additional oversight by introducing higher standards of accountability and transparency, drawing on their international experience and investment practices ( [43]. They act as effective external monitors, leveraging their global expertise and outsider perspective to reduce agency conflicts between managers and shareholders. [44] report that foreign investors actively participate in governance processes to protect the long-term value of their investments. Similarly, Debnath et al. (2021) highlight that well-informed and experienced foreign investors play a critical role in curbing real activity manipulation through close monitoring of managerial actions. Figure 1 highlights the role of ownership structure in non-financial firms listed on the Nairobi Securities Exchange in limiting managers’ opportunistic behavior. Consistent with Agency Theory, high levels of institutional and foreign ownership strengthen monitoring, reduce agency conflicts, and improve earnings quality by aligning managers’ interests with shareholders’ objectives[45]

Source: Research author (2026)

Methods and Materials

The study employed an explanatory research design to investigate the causal relationship between ownership structure and opportunistic real activity manipulation. A positivist philosophical approach guided the research, complemented by both longitudinal and explanatory research designs. The study population comprised all non-financial firms listed on the Nairobi Securities Exchange. These firms were distributed across seven sectors as follows: Agricultural (4), Automobiles and Accessories (1), Commercial and Services (7), Construction and Allied (4), Energy and Petroleum (3), Manufacturing and Allied (6), and Telecommunications and Technology (1). The selection of firms for the study was based on three criteria: (1) continuous operation throughout the study period, (2) availability of complete data, and (3) inclusion of only NSE-listed firms for cross-listed entities, using consolidated reports where applicable. Secondary data were extracted from the audited annual reports of the firms, accessed via their official websites and African Financials. The final sample comprised 416 firm-year observations, representing 26 firms over the period 2008–2023

The measurements and abbreviations for the research variables are presented in Table I.

| Variable | Abbreviation | Measurement | Reference/s |

| Dependent: Opportunistic real activity manipulations | ORAM | ORAM= ABCFO (-1) + ABDISX (-1) + ABPROD | Roychowdhury (2006) |

| Independent Variables: Institutional Ownership Foreign Ownership | IOFO | The proportion of shares owned by the local institutions is divided by the total issued shares. The ratio of shares owned by foreign investors (individual and institutional) to the total number of shares issued | Le & Nguyen, 2023).[46][47][48]. |

| Control Variables: Firm SizeFirm Age | FSZFA | Natural logarithm of firm total assets at the end of the financial yearIs measured by calculating the difference between the current year and the year the firm was incorporated. | Farooq et al., (2022) Bouaziz et al. (2021) |

The study tested the hypotheses using multiple regression analysis. Given the panel nature of the data, the choice between the fixed-effects and random-effects regression models was determined using the Hausman test. Two regression models were estimated: Model 1 included the control variables, while Model 2 examined the main effects of the independent variables on the dependent variable, as presented below.

ORAM it = βo+ β1 FSZit + β2FA it +Yt +Ɛ it………………………………………. Model 1

ORAMit = βo+ C+ β1 MOit + β2IO it + β3FO it + Yt+ Ɛ it………………………. Model 2

Where:

ORAM - Opportunistic Real Activity Manipulation

IO - Institutional Ownership Structure

FO - Foreign Ownership Structure

FA - Firm Age

FS - Firm Size

βo - Intercept

β₁′, β₂′, β₃′- direct effects

Ɛ - Error term

i - firm

t - time

Yt - Year fixed effects (captures the influence of time-specific factors that affect all firms in a given year)

Findings

Before hypothesis testing, several diagnostic tests were conducted to ensure the data met the assumptions of regression analysis.

Panel Unit Root Test

The study tested for unit roots to establish whether the variables were stationary with the aid of the Fisher unit root test [49] and the Im, Pesaran, & Shin (IPS) test [50] to establish the presence or absence of a unit root. The following null and alternative hypotheses were tested.

| Test | Hypothesis |

| Fisher unit root test | Ho: All panels contain a unit rootHa: Panels are stationary |

| Im-Pesaran-Shin (IPS) test | Ho: All panels contain a unit rootHa: Panels are stationary |

Based on the p-values presented in Table 3, all were found to be less than 0.05. Consequently, the null hypothesis of a unit root was rejected, indicating that the time series for all variables is stationary. These results primarily indicate the absence of a unit root in the longitudinal dataset under investigation.

| Variables | Fisher Unit Root Test-Phillips-Perron test | Im-Pesaran-Shin |

| ORAM | -13.0969 | -6.4488 |

| p-value | (0.0000) | (0.0000) |

| Firm Size | -13.8934 | -5.0568 |

| p-value | (0.0000) | (0.0006) |

| Firm Age | -11.0454 | -3.2623 |

| P-value | (0.0000) | (0.0005) |

| IO | -12.5151 | -5.1960 |

| p-value | (0.0000) | (0.0000) |

| FO | -14.2347 | -5.2590 |

| p-value | (0.0000) | (0.0000) |

Source: Research Author (2026)

Normality Assumption

The Shapiro-Wilk test was employed to assess the assumption of normality. As noted by[51] Normality implies that the distribution of the data is symmetrical, with most values concentrated around the mean and relatively fewer observations at the extremes. The results presented in Table 4 indicate that all p-values exceeded the 0.05 significance level. Consequently, the study assumed that the sample data for all variables were drawn from a normally distributed population [52].

| Variable | W | P > Z | |

| Opportunistic Real Activity Manipulations | 0.99714 | 0.68673 | |

| Firm Size | 0.99580 | 0.33278 | |

| Firm Age | 0.99892 | 0.99753 | |

| Institutional Ownership | 0.99816 | 0.93867 | |

| Foreign Ownership | 0.99627 | 0.44054 |

Source: Data Analysis, 2026

Serial Correlation

The Wooldridge test was used to detect serial correlation, as it is suitable for unbalanced panel data and models with a lagged dependent variable. The findings in Table 4 (F = 0.686, p = 0.4513) indicate that the null hypothesis of first-order autocorrelation cannot be rejected, suggesting that the residuals are not autocorrelated.

| Wooldridge test for autocorrelation in panel data |

| H0: no first-order autocorrelation |

| F (1, 25) = 0.686 |

| Prob > F = 0.4153 |

Source: Research Study, 2026

Test for Heteroskedasticity

Heteroskedasticity was tested using the Breusch-Pagan test to check whether the variance of error terms was constant. The null hypothesis assumes homoscedasticity. The results (Chi²(1) = 1.52, p = 0.2808) indicate that the null cannot be rejected, confirming constant variance. The findings are summarized in Table 6

| chi2(1) = 1.52 Prob > chi2 = 0.2808 |

Source: Research Study, 2026

Hausman Test

The Hausman test was conducted to determine the suitability of either the fixed effect or the random effect regression model. The standard hypothesis of this test is that the random effect model estimates the panel data, whereas the alternative hypothesis suggests that the fixed effect model is the appropriate estimator. Based on the chi-square value of 144.542 with a p-value of 0.000, the null hypothesis was rejected, implying that the fixed effect model was the most appropriate model to test the hypotheses.

Descriptive statistics

Table 7 presents descriptive statistics for the independent, dependent, and control variables. The results gave a synopsis of the panel data for the non-financial firms. The study sample contained 26 non-financial firms listed on the Nairobi Securities Exchange and 416 firm-year observations from 2008 to 2023. Based on this table, Opportunistic Real Activity Manipulation had a mean of 0.010 (minimum -0.6152 and maximum = 0.7531; standard deviation = 0.2201). The mean value is consistent with the results documented by [53] and slightly lower than 0.029 reported by [54], who both measured ORAM as a total value of the standardized residuals of ABCFO, ABPROD, and ABDISX. This indicates that both upward and downward ORAM are used by non-financial firms listed on the Nairobi Securities Exchange to increase(reduce) earnings based on their set objectives. According to Roychowdhury (2006), Managers may enact excessive discounts, reduce expenses, and engage in overproduction, leading to lower fixed per unit of a product, hence, to temporarily inflate reported earnings or excessive price discounts and revenue deferral, overstating expenses through increasing discrepancies spending, under production leading to higher fixed per unit of a product hence to temporary deflate reported earnings. Therefore, it indicates that non-financial firms engage in manipulation through inflating and deflating earnings.

The vast range of ORAM from -0.6150 to 0.7531 serves as proof of this. However, most firms tend to lean toward upward earnings manipulation. This was consistent with the findings of Zang (2012) that Managers use a combination of ORAM and accrual-based earnings management, depending on regulatory and market pressures. [55] found that firms, including those in emerging economies, adjusted their ORAM practices in response to the pandemic's economic disruptions, often to meet short-term financial targets. The standard deviation of 0.2201 indicates considerable variation in the level of Opportunistic real activity manipulation across firms. This means that while some firms engage heavily in ORAM, others show little or no evidence of it. These findings are consistent with previous studies. For example, Akter et al. (2024) reported a mean ORAM of 0.03 with a standard deviation of 0.44, and Al-Duais et al. (2022) found a mean of -0.00 and a standard deviation of 0.240.

The institutional ownership mean was 0.4910 (minimum = 0.0323 and maximum = 0.9614; standard deviation = 0.1616). The descriptive analysis shows that the mean share of ownership held by institutional ownership was 49.10%, which was comparable with what was reported by [56], who also measured institutional ownership as the percentage of shares held by local institutional investors, including both financial and non-financial institutions, similar to this study. The mean of foreign ownership structure was 0.4285 (minimum = 0.0050 and maximum = 0.7801; standard deviation = 0.1214). The mean foreign ownership was 0.4285, indicating that, on average, foreign investors held 42.85% of the shares. This is higher than the 37.1% mean reported by Abubakar, Lawal, and Mohamed (2020), who measured foreign ownership as the total percentage of shares held by both foreign individuals and foreign institutional investors. This indicates that non-financial firms listed on the Nairobi Securities Exchange are attractive to foreign investors.

For the control variables, firm age is measured by the number of years since incorporation, with an average of 37 years (minimum = 1.00, maximum = 73.00, standard deviation = 12.4520). The mean value suggests that most firms in the sample are relatively mature. The standard deviation indicates a wide dispersion in firm age, with some firms being newly listed and others having operated for decades. These findings are consistent with those of [57], who reported a mean firm age of 29.54 and a standard deviation of 13.648 in their study on corporate attributes and real earnings management among listed non-financial firms in Nigeria. Firm size had a mean value of 6.8270 (minimum = 5.3032, maximum = 8.3951, standard deviation = 0.5763), indicating considerable variation in size among non-financial firms listed on the Nairobi Securities Exchange. This wide dispersion suggests that firm size is an important factor to control in the study to avoid biased results. Similarly, [58] and [59] found comparable variation in firm size among non-financial firms in the NSE and Asia-Pacific markets, respectively. In this study, firm size was measured as the natural logarithm of total assets.

| Variables | Obs | Min | Max | Mean | Std. Dev. |

| ORAM | 416 | -0.6152 | 0.7531 | 0.0100 | 0.2201 |

| FS | 416 | 5.3032 | 8.3951 | 6.8270 | 0.5763 |

| FA | 416 | 1.0000 | 73.0000 | 37.0528 | 12.4520 |

| IO | 416 | 0.0323 | 0.9614 | 0.4911 | 0.1616 |

| FO | 416 | 0.0500 | 0.7801 | 0.4258 | 0.1214 |

ORAM: Opportunity Real Activity Manipulation, IO: Institutional ownership, F0: Foreign ownership, FS: Firm Size, FA: Firm Age

Source: Researcher, 2026

Correlation Analysis

The study used correlation to examine the nature of the statistical relationship between Opportunistic real activity manipulation, ownership structure attributes, firm age, and firm size. The correlation matrix is illustrated in Table 7, and the results showed that firm age (-0.25), institutional ownership (-0.24), and foreign ownership (-0.21) were significantly negative and moderately correlated to Opportunistic real activity manipulation. This signifies that an increase in firm age, institutional ownership, and foreign ownership leads to a significant decrease in earnings manipulation. Moreover, the table shows that firm size (0.18) has a moderate and significantly positive relationship with Opportunistic real activity manipulation. This indicates that creative earnings management tends to increase with firm size.

| REM | FA | FS | MO | IO | F0 | ACE | FL | |

| ORAM | 1.000 | |||||||

| FA | -0.2520* | 1.000 | ||||||

| FS | 0.1771* | -0.0131 | 1.000 | |||||

| IO | -0.2412* | 0.0040 | -0.0511 | 0.0023 | 1.000 | |||

| F0 | -0.2075* | -0.0472 | 0.0343 | 0.0069 | -0.0816 | 1.000 | ||

| ORAM: Opportunistic Real Activity Manipulations, IO: Institutional ownership, F0: Foreign ownership, FA: Firm Age, FS: Firm Size* Correlation is significant at the 0.05 level (2-tailed). |

Source: Researcher, 2026

Regression Analysis

The null hypothesis was tested using a fixed-effect regression analysis. It stated that institutional ownership structure has no significant effect on opportunistic real activity manipulation on non-financial firms listed in NSE Kenya. The findings reported a beta coefficient of -0.5385 and a p-value = 0.000, p < 0.05. Therefore, the null hypothesis was rejected, and the alternative hypothesis was adopted. This implies that a one-unit increase in institutional ownership is associated with a 0.5385 unit decrease in Opportunistic real activity manipulations. Moreover, Foreign ownership was found to have a significant negative effect on opportunistic real activity manipulation (β = -0.5813, p < 0.05). The 95% confidence interval for the coefficient (0.6978 to -0.4648) does not include zero, confirming the statistical significance of the effect. This indicates that a one-unit increase in foreign ownership is associated with a 0.5813-unit decrease in opportunistic real activity manipulation, illustrating that foreign ownership serves as an effective internal corporate governance mechanism by reducing managers’ opportunistic reporting behaviors in non-financial firms listed on the Nairobi Securities Exchange. The overall regression model had an explanatory power of 0.6337, which implied that the model predicted 63.37% variability in the opportunistic real activity manipulation.

The study found a negative relationship between institutional ownership and opportunistic real activity manipulation, aligning with agency theory. Institutional ownership serves as an internal corporate governance mechanism, helping to monitor management and improve information flow to capital markets [33]. Institutional investors are sophisticated and capable of processing information efficiently (Koh, 2003), which reduces managerial opportunism and agency costs (Sakaki et al., 2017). Their oversight protects shareholders’ wealth and ensures that financial statements present a true and fair view to potential investors.

On the other hand, foreign institutional ownership was found to enhance financial reporting quality. Foreign investors contribute to higher earnings quality through their global experience and ability to apply external knowledge in resolving agency conflicts. This aligns with agency theory, which posits that ownership structure is a key internal control mechanism for mitigating such conflicts. Firms with a higher proportion of foreign investors are therefore more likely to provide reliable financial information to shareholders (Tran et al., 2023).

| Variable | Model 1 Coff(p-value) | Model 2 Coff(p-value) | [95% Conf.Interval] | |

| F size | 0.072(0.000) | 0.075(0.000) | 0.0558 | 0.0932 |

| F age | -0.004(0.003) | -0.004(0.000) | -0.0046 | -0.0028 |

| IO | -0.539 (0.000) | -0.6712 | -0.4059 | |

| FO | -0.581(0.000) | -0.6978 | -0.4648 | |

| R2 | 0.0960 | 0.6337 | ||

| P> Ch2 | 0.000 | 0.000 | ||

| No. of observation | 416 | 416 |

Source: Authors’ compilation

Conclusion and Recommendations

The study shows that institutional and foreign ownership significantly reduce opportunistic real activity manipulation among non-financial firms listed on the Nairobi Securities Exchange. Higher shareholding levels strengthen monitoring and align managerial actions with shareholders’ interests, consistent with Agency Theory. Firms and regulators should promote active institutional and foreign investor participation, enhance transparency, strengthen internal monitoring, and implement safeguards for minority shareholders to ensure ownership structures effectively deter opportunistic managerial behavior and improve financial reporting quality.

References

- AL-Duais Shaker Dahan, Malek Mazrah, Abdul Hamid Mohamad Ali, Almasawa Amal Mohammed Ownership structure and real earnings management: evidence from an emerging market Journal of Accounting in Emerging Economies Emerald Group Holdings Ltd. 12(2) DOI ↗ Google Scholar ↗

- Gunny Katherine A. The relation between earnings management using real activities manipulation and future performance: Evidence from meeting earnings benchmarks Contemporary Accounting Research 27(3) DOI ↗ Google Scholar ↗

- Roychowdhury Sugata Earnings management through real activities manipulation Journal of Accounting and Economics 42(3) DOI ↗ Google Scholar ↗

- Siraji M., Nazar M. C. A. How do Family and Managerial Ownership Structure Effect Real Earnings Management? Asian Journal of Economics, Business and Accounting 21(7) DOI ↗ Google Scholar ↗

- Dechow Patricia M., Skinner Douglas J. Earnings Management: Reconciling the Views of Accounting Academics, Practitioners, and Regulators SSRN Electronic Journal DOI ↗ Google Scholar ↗

- Habib Ahsan, Ranasinghe Dinithi, Wu Julia Yonghua, Biswas Pallab Kumar, Ahmad Fawad Real earnings management: A review of the international literature Accounting and Finance 62(4) DOI ↗ Google Scholar ↗

- Kim;J.B.&, Sohn;B.C. Real earnings management and cost of capital , Journal of Accounting and Public Policy, 32(6) 2013 DOI ↗ Google Scholar ↗

- Indarti Maria Goreti Kentris, Widiatmoko Jacobus The Effects of Earnings Management and Audit Quality on Cost of Equity Capital: Empirical Evidence from Indonesia Journal of Asian Finance, Economics and Business 8(4) DOI ↗ Google Scholar ↗

- Cornett Marcia Millon, McNutt Jamie John, Tehranian Hassan Earnings Management at Large US Bank Holding Companies SSRN Electronic Journal (January) DOI ↗ Google Scholar ↗

- Healy, P. M., & Wahlen J. M. A review of the earnings management literature and its implications for standard setting. Accounting Horizons 19(4) 2005 DOI ↗ Google Scholar ↗

- PWC The PwC Global Economic Crime and Fraud Survey 2023 DOI ↗ Google Scholar ↗

- Ghaleb Belal Ali Abdulraheem, Qaderi Sumaia Ayesh, Almashaqbeh Ahmad, Qasem Ameen Corporate social responsibility, board gender diversity and real earnings management: The case of Jordan Cogent Business and Management Cogent 8(1) DOI ↗ Google Scholar ↗

- KPMG Profile of a Fraudster 2024 DOI ↗ Google Scholar ↗

- Eberechukwu Mary, Etim Okoi, Ehis Stella, Ndubuisi Geoffrey, Clifford Azubuike, Ukamaka Faith, Chukwuka Peter Creative Accounting and Investor Value : A Comparative Study of Income Smoothing of Listed Manufacturing Firms in Nigeria and South Africa (1989) DOI ↗ Google Scholar ↗

- Muchoki G. W. The Relationship Between Corporate Governance Practices And Earnings Management For Companies Quoted At The Nairobi Securities Exchange 2013 DOI ↗ Google Scholar ↗

- Omondi Kennedy EARNINGS MANAGEMENT AND FINANCIAL PERFORMANCE OF COMPANIES LISTED WITH NSE IN KENYA . KENNEDY OMONDI JUMA A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENT FOR THE AWARD OF THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION ( MBA ) ACCOUNTING OPTION , THE UNIVERSITY OF NAIROBI . 2022 DOI ↗ Google Scholar ↗

- Oladipo Olufemi, Shittu Saheed Akande, Oladipo Olufemi Adebayo Nexus Between Real Earnings Management (REM) and Company's Profitability? An Empirical Analysis of Listed Non-Financial Companies in Sub-Saharan Africa 3(January) DOI ↗ Google Scholar ↗

- Mardnly Zukaa, Mouselli Sulaiman, Abdulraouf Riad Corporate governance and firm performance: an empirical evidence from Syria International Journal of Islamic and Middle Eastern Finance and Management 11(4) DOI ↗ Google Scholar ↗

- Kenya Kenya’s Code of Corporate Governance 2021 DOI ↗ Google Scholar ↗

- Maina et al. 2023 AMONG QUOTED NON-FINANCIAL COMPANIES AT NAIROBI 3(03) 2025 DOI ↗ Google Scholar ↗

- Salehi Mahdi, Zimon Grzegorz, Arianpoor Arash, Gholezoo Fatemeh Eidi The Impact of Investment Efficiency on Firm Value and Moderating Role of Institutional Ownership and Board Independence Journal of Risk and Financial Management 15(4) DOI ↗ Google Scholar ↗

- U.S.A SEC No Title 2022 DOI ↗ Google Scholar ↗

- JSE Finan 2024 DOI ↗ Google Scholar ↗

- Tanzani Daily News Daily News Tanzania, 2022 DOI ↗ Google Scholar ↗

- C.M.A C 2021 DOI ↗ Google Scholar ↗

- Habib Ahsan, Ranasinghe Dinithi, Yonghua Julia, Kumar Pallab, Fawad Biswas Real earnings management : A review of the international literature Accounting and Finance 62 DOI ↗ Google Scholar ↗

- Nasirbinti, N.A.M., Ali, M.J., Razzaque, R.M.R. and Ahmed K. Real earnings management and financial statement fraud: evidence from Malaysia International Journal of Accounting and Information Management 26(4) 2019 DOI ↗ Google Scholar ↗

- Tohang Valentina, Hutagaol-Martowidjojo Yanthi, Pirzada Kashan The Link Between ESG Performance and Earnings Quality Australasian Accounting, Business and Finance Journal 18(1) DOI ↗ Google Scholar ↗

- Rahman R A, Suffian M T M, Ghani E K, Said J, Ahmad I Managerial ownership and real earnings management: A study on interaction effect of religiosity Journal of Management Information and Decision Sciences 24(6) 2021 DOI ↗ Google Scholar ↗

- Cohen, D. A., & Zarowin P. Accrual-based and real earnings management activities around seasoned equity offerings. Journal of Accounting and Economics 50(1) 2010 DOI ↗ Google Scholar ↗

- Md. Abdul Kaium Masud1, 2, Mohammad Nurunnabi3 4 and Seong Mi Bae1*, Access Open, * The effects of corporate governance on environmental sustainability reporting: empirical evidence from South Asian countries Asian Journal of Sustainability and Social Responsibility Asian Journal of Sustainability and Social Responsibility 3(3) DOI ↗ Google Scholar ↗

- Fatima Huma, Haque Abdul, Usman Muhammad Is there any association between real earnings management and crash risk of stock price during uncertainty? An evidence from family-owned firms in an emerging economy Future Business Journal Springer Berlin Heidelberg 6(1) DOI ↗ Google Scholar ↗

- Saona, P., Muro, L., And, Alvarado M “How do the ownership structure and board of directors’ features impact earnings management? The Spanish case”, Journal of International Financial Management and Accounting 31(1) 2020 DOI ↗ Google Scholar ↗

- Bosse, D. A., & Phillips R. A. AGENCY THEORY AND BOUNDED SELF-INTEREST Author ( s ): DOUGLAS A . BOSSE and ROBERT A . PHILLIPS Source : The Academy of Management Review , Vol . 41 , No . 2 ( April 2016 ), pp . 276-297 Published by : Academy of Management Stable URL : DOI ↗ Google Scholar ↗

- Victoravich Lisa M., Xu Pisun, Gan Huiqi Institutional ownership and executive compensation: Evidence from US banks during the financial crisis Managerial Finance 39(1) DOI ↗ Google Scholar ↗

- Darmadi Salim, Sodikin Achmad Information disclosure by family-controlled firms: The role of board independence and institutional ownership Asian Review of Accounting 21(3) DOI ↗ Google Scholar ↗

- Dahlquist Magnus, Robertsson Göran Direct foreign ownership, institutional investors, and firm characteristics Journal of Financial Economics 59(3) DOI ↗ Google Scholar ↗

- Guo, J., Huang, P., Zhang, Y. and Zhou N. “Foreign ownership and real earnings management: evidence from Japan”, Journal of International Accounting Research, 14(2) 2015 DOI ↗ Google Scholar ↗

- Roodposhti, F. R., & Chashmi S. N. The impact of corpo- rate governance mechanisms on earnings management. African Journal of Business Management 5(11) 2011 DOI ↗ Google Scholar ↗

- Abubakar, I., Abaukaka, T.O., & Momoh M.K.O. Implications of free trade area for poverty, household welfare and economic development in Nigeria. International Journal of Social Sciences and Economic Review, 3(3) 2021 DOI ↗ Google Scholar ↗

- Afreen M. Transition assessment of the bangladeshi financial market stress regimes: a markov switching modeling approach. Innovation Journal of Social Sciences and Economic Review 31(1) 2021 DOI ↗ Google Scholar ↗

- Piosik Andrzej, Genge Ewa The influence of a company's ownership structure on upward real earnings management Sustainability (Switzerland) 12(1) DOI ↗ Google Scholar ↗

- AL-Duais Shaker Dahan, Malek Mazrah, Abdul Hamid Mohamad Ali, Almasawa Amal Mohammed Ownership structure and real earnings management: evidence from an emerging market Journal of Accounting in Emerging Economies 12(2) DOI ↗ Google Scholar ↗

- Ahmed Anwer S., Iwasaki Takuya Foreign ownership, appointment of independent directors, and firm value: Evidence from Japanese firms Journal of International Accounting, Auditing and Taxation 43 DOI ↗ Google Scholar ↗

- Nguyen, H. A., Nguyen, H. L., Doan D. T. Ownership structure and earnings management: Empirical evidence from Vietnam real estate sector. Real Estate Management and Valuation, 28(2) 2020 DOI ↗ Google Scholar ↗

- Yousef ALGHADI Mohammad, Radwan Al NSOUR Ibrahim, Ahmad Khalifah AlZYADAT Ayed Ownership Structure and Cash Holdings: Empirical Evidence from Saudi Arabia Ayed Ahmad Khalifah AlZYADAT / Journal of Asian Finance 8(7) DOI ↗ Google Scholar ↗

- Tulcanaza-Prieto Ana Belen, Lee Younghwan, Koo Jeong Ho Effect of leverage on real earnings management: Evidence from Korea Sustainability (Switzerland) 12(6) DOI ↗ Google Scholar ↗

- Shayan-Nia Mojtaba, Sinnadurai Philip, Mohd-Sanusi Zuraidah, Hermawan Ancella NIa Anitawati How efficient ownership structure monitors income manipulation? Evidence of real earnings management among Malaysian firms Research in International Business and Finance 41 DOI ↗ Google Scholar ↗

- Maddala G. S., Wu Shaowen A comparative study of unit root tests with panel data and a new simple test Oxford Bulletin of Economics and Statistics 61(SUPPL.) DOI ↗ Google Scholar ↗

- Im Kyung So, Pesaran M. Hashem, Shin Yongcheol Testing for unit roots in heterogeneous panels Journal of Econometrics 115(1) DOI ↗ Google Scholar ↗

- Casson Robert J., Farmer Lachlan D.M. Understanding and checking the assumptions of linear regression: A primer for medical researchers Clinical and Experimental Ophthalmology 42(6) DOI ↗ Google Scholar ↗

- Wilk S. S. Shapiro and M. B. An Analysis of Variance Test for Normality 52(3) 1965 DOI ↗ Google Scholar ↗

- Alghemary, M., Al-Najjar, B. and Polovina N. What do we know about real earnings management in the GCC? Journal of Accounting in Emerging Economies 14(3) DOI ↗ Google Scholar ↗

- Ahmad Abubakar, Ahmad Lawal Mohamed, Mohamed Ownership Structure and Real Earnings Management: Evidence from Nigeria Journal of Management Theory and Practice (JMTP) 1(3) DOI ↗ Google Scholar ↗

- Al-Begali Safia Abdo Ali, Phua Lian Kee Earnings management in emerging markets: The COVID-19 and family ownership Cogent Economics and Finance Cogent 11(1) DOI ↗ Google Scholar ↗

- Davis Justin G., García-Cestona Miguel Institutional ownership, earnings management and earnings surprises: evidence from 39 years of U.S. data Journal of Economics, Finance and Administrative Science 28(56) DOI ↗ Google Scholar ↗

- Ibok Rose Augustine Odokwo* Nkanikpo, Ukpong Eno Gregory Corporate attributes and earnings management of non financial firms listed on the Nigeria exchange limited Journal of Global … 2(3) 2024 DOI ↗ Google Scholar ↗

- Wilkins Ochieng' Wayongah Daniel Firm Size and Firm Financial Performance: Panel Evidence From Non- Financial Firms in Nairobi Securities Exchange, Kenya International Journal of Social Sciences and Information Technology 4(7) 2019 DOI ↗ Google Scholar ↗

- Yadav Inder Sekhar, Pahi Debasis, Gangakhedkar Rajesh The nexus between firm size, growth and profitability: new panel data evidence from Asia–Pacific markets European Journal of Management and Business Economics 31(1) DOI ↗ Google Scholar ↗