Abstract

Behavioral finance research has extensively examined investment decision-making and investor biases; however, limited attention has been devoted to understanding how individuals develop enduring investor identities. This study aims to develop a substantive theory explaining the process through which investor identities emerge through the interaction of financial knowledge and locus of control. Adopting a constructivist grounded theory approach, data were collected through in-depth interviews with 22 active individual investors selected through purposive and theoretical sampling. Data analysis followed the constant comparative method involving initial coding, focused coding, and theoretical integration. The findings reveal that investor identity formation is a progressive and iterative process consisting of five interconnected stages: exposure and curiosity, knowledge acquisition, outcome interpretation, behavioral adaptation, and identity consolidation. Financial knowledge functions as a cognitive resource that enhances investors’ capacity to evaluate information and reflect on experiences, whereas locus of control operates as an interpretive mechanism through which investment outcomes are assigned meaning. Through repeated cycles of learning and adaptation, investors develop relatively stable identities, including risk-averse, explorer, trader, and contrarian orientations. The study proposes the Investor Identity Formation Framework (IIFF), extending behavioral finance literature by shifting attention from investment decisions to the developmental processes through which investors become distinct market participants.

Keywords

Investor identity Behavioral finance Financial knowledge Locus of control.

1. Introduction

The rapid expansion of digital financial ecosystems has fundamentally transformed the nature of investing (Yavuz et al., 2025). Online brokerage platforms, mobile trading applications, social media communities, and real-time financial information have reduced traditional barriers to market participation, allowing individuals from diverse educational and professional backgrounds to engage directly in investment activities (Rao et al., 2025). Investing is no longer an exclusive domain of financial professionals; it has become an increasingly common aspect of everyday economic life (Koskelainen et al., 2023). Paradoxically, greater accessibility to financial markets has not necessarily resulted in greater uniformity in investor behavior (W. Chen et al., 2026). Individuals exposed to similar information, market conditions, and investment opportunities frequently exhibit remarkably different decision-making patterns (Shunmugasundaram & Sinha, 2025). Some investors prioritize capital preservation and adopt highly conservative strategies, while others actively pursue speculative opportunities despite substantial uncertainty (Marjerison et al., 2025). Such heterogeneity raises an important question: why do individuals develop fundamentally different orientations toward investing even when they operate within similar financial environments?

Traditional finance theories explain investment behavior through assumptions of rationality, suggesting that individuals systematically process information and select alternatives that maximize expected utility (Mahmood et al., 2024). While elegant in their mathematical formulation, these models often struggle to explain persistent behavioral inconsistencies observed in real-world financial markets. Investors routinely overreact to market news, follow speculative trends, hold losing assets for extended periods, or exhibit excessive confidence in their judgments (Wang, 2026). Behavioral finance emerged partly as a response to these limitations by emphasizing the role of psychological factors, cognitive biases, emotions, and subjective interpretations in financial decision-making. Although behavioral finance has significantly advanced understanding of investor behavior, much of the literature remains focused on identifying determinants of investment decisions rather than explaining how individuals gradually become particular types of investors (Ahmad, 2025). Existing studies frequently classify investors into categories such as risk-averse investors, traders, explorers, or contrarian investors (Addo et al., 2025; Jia, 2026; Marjerison et al., 2025). While these classifications are useful for describing behavioral outcomes, they often treat investor identities as if they were pre-existing characteristics rather than socially and psychologically constructed phenomena. In other words, the literature is highly effective at labeling investors but considerably less effective at explaining how those labels emerge in the first place (Gunawan, 2024).

Similarly, financial knowledge has been widely recognized as a key determinant of investment competence and financial well-being (Soumya & Padmavathi, 2025). Individuals with higher levels of financial literacy generally demonstrate superior risk assessment and decision-making capabilities (Rehman & Mia, 2024). At the same time, research on locus of control suggests that individuals differ substantially in how they attribute success and failure, with important implications for learning, adaptation, and risk-taking behavior (Zapryanova & Radeva, 2025). However, these streams of research have largely evolved in parallel. Existing studies typically examine the direct effects of financial knowledge or locus of control on investment outcomes, while paying limited attention to the dynamic processes through which these factors interact to shape investor self-perceptions and behavioral identities over time (Kumar et al., 2023). This omission is particularly important because investment behavior is not merely a series of isolated decisions. It is an ongoing process of learning, interpretation, adaptation, and self-definition (Grinblatt & Keloharju, 2000). Investors continuously evaluate market experiences, attribute outcomes to internal or external causes, and adjust their understanding of who they are as market participants (Kurniawati et al., 2022). Yet the mechanisms through which such experiences culminate in stable investor identities remain insufficiently understood.

To address this gap, the present study adopts a constructivist grounded theory approach to investigate how financial knowledge and locus of control contribute to investor identity formation. Rather than testing predetermined causal relationships, this research seeks to develop a substantive theory explaining the processes through which individuals evolve into distinct types of investors. By shifting attention from investor categories to the formation of investor identities, this study contributes a deeper understanding of behavioral heterogeneity within contemporary financial markets.

2. Literature Review

2.1 Behavioral Finance Perspective

Behavioral finance emerged as a response to the limitations of traditional finance theories that assume investors behave rationally and consistently maximize expected utility (Corzo et al., 2024). While classical models suggest that investment decisions are driven by objective

assessments of risk and return, empirical evidence has repeatedly demonstrated that investor behavior often deviates from these assumptions. Investors frequently exhibit overconfidence, loss aversion, herding tendencies, and other cognitive biases that influence decision-making under uncertainty (Sood et al., 2023).

Rather than viewing investors as purely rational actors, behavioral finance recognizes that investment decisions are shaped by the interaction of cognition, emotion, experience, and social influence (Rasa, 2024). Market participants interpret the same information differently depending on their beliefs, prior experiences, and personal judgments (Almansour et al., 2023). Consequently, investment behavior reflects not only market conditions but also subjective meanings attached to those conditions.

Despite its substantial contributions, behavioral finance has largely focused on identifying behavioral biases and explaining investment outcomes (Cheng, 2022). Much of the literature examines why investors make particular decisions, but less attention has been devoted to understanding how individuals gradually develop enduring orientations toward investing (Gethe et al., 2022). Investors are often categorized according to observable behaviors, yet the developmental processes that produce those behavioral patterns remain insufficiently understood.

This limitation suggests that investor behavior should not be viewed solely as a consequence of isolated psychological biases (Gupta & Goswami, 2024). Instead, it may represent the outcome of a longer process involving learning, interpretation, and adaptation. Understanding this process requires attention to how investors construct meanings from their experiences and eventually develop relatively stable investor identities(Cho & Jung, 2024; Gupta & Goswami, 2024)

2.2 Financial Knowledge

Financial knowledge refers to an individual's understanding of financial concepts, investment instruments, market mechanisms, and risk-return relationships (Padi et al., 2025). Extensive research has identified financial knowledge as a key factor influencing investment participation, portfolio quality, and financial well-being. Individuals with higher levels of financial literacy are generally better equipped to evaluate investment alternatives, process financial information, and avoid common decision-making errors (Darwish, 2025).

However, evidence also suggests that financial knowledge alone cannot fully explain variations in investor behavior (Yusup & Jasuni, 2024). Individuals with comparable levels of knowledge often pursue markedly different investment strategies. Some emphasize capital preservation and long-term stability, while others actively seek speculative opportunities despite possessing similar informational resources (Lusardi, 2019). These differences indicate that knowledge does not automatically translate into uniform behavior.

Recent studies increasingly recognize that financial knowledge functions not only as a source of information but also as a resource that shapes individual confidence, judgment, and decision-making approaches (Ardhiani & Panjaitan, 2023). Through learning and experience, investors develop perceptions regarding their own competence and capabilities within financial markets (Nogueira et al., 2025). Consequently, knowledge acquisition may contribute to broader processes of self-definition rather than merely improving technical decision-making skills.

Nevertheless, existing research has primarily examined the direct relationship between financial knowledge and investment outcomes (Aristei & Gallo, 2021; Morris et al., 2022). Comparatively little attention has been devoted to understanding how financial knowledge contributes to the emergence of distinct investor identities. As a result, the mechanisms through

which learning experiences shape investor self-perceptions remain insufficiently explored (F. Chen et al., 2022).

2.3 Locus of Control

Locus of control describes the extent to which individuals believe that outcomes are determined by their own actions or by external circumstances (Mendoza-Ávila et al., 2025). Individuals with an internal locus of control tend to perceive success and failure as consequences of personal effort, skill, and decision-making . In contrast, those with an external locus of control are more likely to attribute outcomes to luck, market conditions, or other forces beyond their control(Nawang et al., 2024)

Within investment contexts, locus of control influences how investors interpret uncertainty, evaluate outcomes, and respond to financial gains or losses. Investors with stronger internal control orientations are generally more inclined to learn from experience, modify strategies, and accept responsibility for investment outcomes (Busseri et al., 1998; Nalurita et al., 2023). Conversely, external control orientations may encourage individuals to view outcomes as largely unpredictable, reducing incentives for behavioral adaptation.

Previous studies have linked locus of control to investment participation, risk tolerance, portfolio management, and financial planning behavior (Rahmawati et al., 2023). These findings suggest that attribution patterns play an important role in shaping financial decision-making. However, existing research has largely treated locus of control as an antecedent of behavior rather than as a mechanism through which investors construct meanings from their experiences(Nisula & Olander, 2025)

This distinction is important because investing involves repeated cycles of success, failure, and reflection (Szabó-Morvai & Kiss, 2024). Over time, the ways individuals explain these experiences may influence how they perceive themselves as investors. Yet current literature provides limited understanding of how locus of control contributes to the development of enduring investor identities. Exploring this process offers an opportunity to better understand the psychological foundations of investor heterogeneity (Selart, 2005)

2.4 Investor Identity

Investor identity refers to the self-perception individuals develop regarding their role, competence, and orientation within investment activities. Unlike traditional classifications that focus on observable behavior, an identity perspective emphasizes how individuals understand and define themselves as market participants. These self-definitions influence how investors interpret opportunities, evaluate risks, and respond to market outcomes (Rogers et al., 2026). Identity is generally viewed as a dynamic and evolving construct shaped through experience and social interaction (Mongan et al., 2025). Within financial markets, investors are continuously exposed to information, uncertainty, success, and failure. Through these experiences, they gradually develop narratives about their capabilities, preferred strategies, and positions within the investment environment. Such narratives may eventually crystallize into relatively stable investor identities (Monk & Rook, 2023).

Although behavioral finance research has identified various investor types, including risk-averse, trader, explorer, and contrarian investors, these categories are often treated as descriptive outcomes rather than developmental phenomena (Smith & Bergman, 2020). Existing studies explain differences among investors but provide limited insight into how those differences emerge over time. Consequently, investor identities are frequently assumed rather than explained (Kelley & Woidtke, 2006).

This gap is particularly important because investment behavior is not static. Investors continuously learn, interpret outcomes, and adapt their actions in response to changing circumstances. Understanding investor identity therefore requires attention to the processes through which individuals transform investment experiences into enduring self-perceptions (Mongan et al., 2025; Rogers et al., 2026). This study addresses that gap by developing a grounded theory explaining how investor identities are formed through the interaction of financial knowledge and locus of control.

3. Methodology

This study employed a constructivist grounded theory approach to develop a substantive theory explaining how investor identities emerge through the interaction of financial knowledge and locus of control (Ugwu & Val, 2023). This approach was considered appropriate because existing literature provides limited explanations regarding the processes through which individuals become particular types of investors. Rather than testing predetermined hypotheses, the study sought to generate theory grounded in participant lived experiences(Oranga & Matere, 2023)

Participants consisted of individual investors who had actively invested for at least two years. Purposive sampling was initially used to ensure variation in age, investment experience, financial literacy, risk preference, and investment instruments. As analysis progressed, theoretical sampling guided the selection of additional participants to elaborate emerging concepts and relationships. Data collection continued until theoretical saturation was achieved, resulting in 22 participants.

Data were collected through semi-structured, in-depth interviews lasting between 60 and 90 minutes. Interview questions explored participants’ investment journeys, learning experiences, interpretations of gains and losses, risk perceptions, and beliefs regarding the determinants of investment outcomes (McGrath et al., 2019). All interviews were recorded, transcribed verbatim, and analyzed concurrently with data collection.

Data analysis followed the constant comparative method. Initial coding (Table 1) was conducted to identify recurring actions, meanings, and experiences. Related codes were subsequently grouped into broader conceptual categories through focused coding. Finally, theoretical integration was undertaken to develop an explanatory framework describing the process of investor identity formation. Throughout the analysis, analytic memos were maintained to capture theoretical insights and guide category development.

To enhance trustworthiness, the study employed iterative data collection and analysis, reflexive memo writing, and an audit trail documenting analytical decisions. These procedures contributed to the credibility, dependability, and transparency of the resulting theory.

| Initial Codes | Focused Codes | Category | Theoretical Stage |

| Following friends' investment recommendations | Social exposure | Initial market exposure | Exposure and Curiosity |

| Watching investment content on YouTube | Media-driven curiosity | Initial market exposure | Exposure and Curiosity |

| Joining investment communities | Social learning trigger | Initial market exposure | Exposure and Curiosity |

| Fear of missing investment opportunities | Opportunity awareness | Initial market exposure | Exposure and Curiosity |

| Reading investment books | Self-directed learning | Financial learning activities | Knowledge Acquisition |

| Attending investment seminars | Formal learning | Financial learning activities | Knowledge Acquisition |

| Learning from experienced investors | Experiential learning | Financial learning activities | Knowledge Acquisition |

| Understanding risk-return relationships | Financial competence development | Financial learning activities | Knowledge Acquisition |

| Evaluating past investment mistakes | Reflective evaluation | Outcome interpretation | Outcome Interpretation |

| Analyzing reasons for investment success | Attribution process | Outcome interpretation | Outcome Interpretation |

| Revising investment strategies after losses | Behavioral adaptation | Outcome interpretation | Outcome Interpretation |

| Learning from market experiences | Experiential reflection | Outcome interpretation | Outcome Interpretation |

| Believing success depends on personal analysis | Internal attribution | Locus of control mechanism | Outcome Interpretation |

| Viewing losses as learning opportunities | Internal attribution | Locus of control mechanism | Outcome Interpretation |

| Attributing outcomes to market conditions | External attribution | Locus of control mechanism | Outcome Interpretation |

| Attributing outcomes to luck | External attribution | Locus of control mechanism | Outcome Interpretation |

| Prioritizing capital preservation | Conservative orientation | Investor identity | Identity Consolidation |

| Seeking emerging opportunities | Opportunity-seeking orientation | Investor identity | Identity Consolidation |

| Focusing on short- term price movements | Trading orientation | Investor identity | Identity Consolidation |

| Challenging market consensus | Contrarian orientation | Investor identity | Identity Consolidation |

Source: Authors' analysis based on interview data

4. Findings

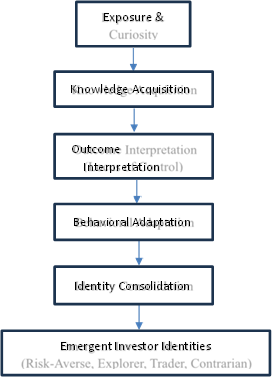

Analysis revealed that investor identity formation is a progressive process through which individuals transform from passive market observers into investors with distinct behavioral orientations. This process consists of four interconnected stages: exposure and curiosity, knowledge acquisition, outcome interpretation, and identity consolidation.

| Category | Properties | Consequences |

| Exposure and Curiosity | Social influence, media exposure, investment awareness | Initial market participation |

| Knowledge Acquisition | Learning, financial literacy, market understanding | Increased analytical capability |

| Outcome Interpretation | Attribution, reflection, adaptation | Meaning construction from experiences |

| Identity Consolidation | Stable beliefs, preferred strategies, behavioral consistency | Emergence of investor identity |

| Core Category: Investor Identity Formation | Continuous interaction between knowledge and locus of control | Development of Risk- Averse, Explorer, Trader, and Contrarian identities |

Source: Authors' analysis based on interview data

Stage 1: Exposure and Curiosity

The process began when participants were exposed to investing through social networks, financial media, educational programs, or online communities. At this stage, investing was perceived primarily as an opportunity rather than a structured financial activity. Participants reported curiosity regarding potential returns but possessed limited understanding of market mechanisms and investment risks.

Initial engagement was largely exploratory and strongly influenced by external stimuli. Investment decisions were often based on recommendations from peers, social trends, or highly visible market narratives. Consequently, participants entered financial markets without a clearly defined investor orientation.

Stage 2: Knowledge Acquisition

As market participation increased, participants gradually accumulated financial knowledge through formal education, self-directed learning, practical experience, and interactions with other investors. Knowledge acquisition enabled participants to move beyond speculative assumptions and develop a more systematic understanding of investment opportunities and risks.

However, the findings suggest that financial knowledge did not directly determine investor identity. Instead, knowledge functioned as a cognitive resource that expanded participants' capacity to evaluate information, justify decisions, and reflect upon market experiences. Investors with comparable levels of knowledge frequently demonstrated different behavioral tendencies, indicating that knowledge alone was insufficient to explain identity formation.

Stage 3: Outcome Interpretation

Differences in identity development became more apparent through participants' interpretations of investment outcomes. Repeated experiences of gains and losses prompted participants to construct explanations regarding the causes of financial success and failure.

Participants exhibiting stronger internal locus of control generally interpreted outcomes as consequences of their own decisions and analytical capabilities. These individuals actively evaluated mistakes, revised strategies, and viewed unsuccessful investments as learning opportunities. In contrast, participants with stronger external orientations were more likely to attribute outcomes to luck, market volatility, or uncontrollable external conditions. As a result, learning processes and behavioral adaptation occurred unevenly across participants despite similar market experiences.

The findings indicate that locus of control operated as a critical interpretive mechanism linking investment experiences to behavioral development.

Stage 4: Identity Consolidation

Over time, recurring patterns of knowledge utilization and outcome interpretation produced relatively stable investor identities. Participants developed consistent beliefs regarding how markets should be approached, how risks should be managed, and what constituted successful investing.

Four dominant identities emerged from the data. Risk-averse investors prioritized capital preservation and stability. Explorer investors continuously searched for new opportunities and emerging sectors. Trader investors emphasized market timing and short-term opportunities, whereas contrarian investors deliberately challenged prevailing market sentiment and sought opportunities overlooked by others.

These identities did not emerge from demographic characteristics or financial knowledge alone. Rather, they represented the cumulative outcome of learning processes, attribution patterns, and behavioral adaptation developed through sustained market participation.

Collectively, the findings suggest that investor identity formation is an iterative process in which financial knowledge provides interpretive resources, locus of control shapes the meaning assigned to investment outcomes, and repeated adaptation gradually produces stable investor identities. This process is summarized in the Investor Identity Formation Framework (IIFF).

Source: Authors' grounded theory analysis.

5. Discussion

5.1 Financial Knowledge as a Resource Rather Than a Determinant

The dominant assumption within financial literacy research is that greater financial knowledge leads to better investment decisions and, by implication, more sophisticated investor behavior. While this assumption has received substantial empirical support, the present findings suggest that it may be theoretically incomplete. Participants possessing comparable levels of financial knowledge frequently developed markedly different investment orientations, ranging from highly conservative approaches to active trading and opportunity-seeking behaviors.

This finding indicates that financial knowledge alone cannot adequately explain investor heterogeneity. Knowledge provides informational resources, but it does not determine how those resources are interpreted, prioritized, or translated into behavior. Consequently, the widespread tendency to equate higher financial literacy with more predictable investment behavior risks oversimplifying the complexity of investor development.

The findings therefore challenge the implicit linear logic that underpins much of the financial literacy literature. Rather than functioning as a determinant of investor identity, financial knowledge appears to operate as a resource that investors mobilize differently when confronted with uncertainty, success, and failure. This perspective helps explain why similar levels of knowledge often produce substantially different behavioral outcomes.

More importantly, the findings suggest that knowledge acquisition should be viewed not merely as a process of information accumulation but also as a process of self-construction. Investors learn about financial markets while simultaneously developing understandings of who they are within those markets. As such, investor identity emerges not from knowledge itself but from the meanings individuals derive from the application of that knowledge.

5.2 Locus of Control as an Interpretive Mechanism

Previous studies have consistently demonstrated that locus of control influences financial behavior, risk tolerance, and investment participation. However, much of this literature treats locus of control as a relatively stable psychological predictor that directly affects behavioral outcomes. The present findings suggest a more fundamental role.

The analysis indicates that locus of control operates as the mechanism through which investors interpret and assign meaning to financial experiences. Market outcomes rarely provide clear evidence regarding the quality of investment decisions. Gains may result from skill or luck, while losses may reflect poor decisions or unfavorable market conditions. Consequently, investors must construct explanations that allow them to understand these outcomes and decide how to respond.

Participants with stronger internal control orientations tended to interpret outcomes as consequences of their own decisions, encouraging reflection, learning, and strategic adaptation. In contrast, participants with stronger external orientations frequently attributed outcomes to forces beyond their control, limiting opportunities for behavioral adjustment. This difference suggests that the critical issue is not whether investors experience success or failure, but how they explain those experiences.

The findings therefore extend existing locus of control research by repositioning the construct from a behavioral predictor to an interpretive mechanism. Investor development appears to depend less on objective outcomes than on the narratives individuals construct around those outcomes. Through repeated cycles of interpretation and adaptation, these narratives gradually shape enduring investor identities.

5.3 Investor Identities as Emergent Outcomes

Behavioral finance literature frequently categorizes investors as risk-averse investors, traders, explorers, or contrarian investors. While these classifications have generated valuable insights regarding behavioral differences, they often assume the existence of relatively stable investor types. Such an approach implicitly treats investor identity as a starting condition rather than an outcome requiring explanation.

The present findings challenge this assumption. Participants did not enter financial markets as traders, explorers, or contrarians. Instead, these identities emerged gradually through repeated interactions with market opportunities, investment outcomes, and personal learning experiences. Investor identities were therefore not pre-existing characteristics but products of ongoing developmental processes.

This distinction is theoretically significant because it shifts attention from classification to emergence. Existing studies are highly effective at describing differences among investors but considerably less effective at explaining how those differences originate. By focusing on identity formation, the present study addresses a question that has received surprisingly limited attention despite its relevance to behavioral finance.

The findings suggest that investor categories should be understood as temporary outcomes of learning, interpretation, and adaptation rather than fixed personal attributes. Such a perspective provides a deeper explanation for investor heterogeneity and challenges the tendency to treat behavioral classifications as self-evident realities. In doing so, the study moves beyond descriptive typologies toward a process-based understanding of investor development.

5.4 From Behavioral Finance to Investor Identity Formation

The broader implication of this study concerns the scope of behavioral finance itself. For several decades, behavioral finance has focused primarily on explaining why investors make irrational or inconsistent decisions. Concepts such as overconfidence, loss aversion, and herding behavior have substantially improved understanding of decision-making anomalies. Nevertheless, these explanations largely concentrate on individual decisions rather than on the processes through which investors develop enduring behavioral orientations.

The Investor Identity Formation Framework (IIFF) offers a different perspective. Rather than viewing investment behavior as a sequence of isolated decisions, the framework conceptualizes investing as a developmental process involving learning, interpretation, adaptation, and identity construction. From this perspective, behavioral differences among investors are not simply manifestations of cognitive biases but reflections of distinct identity trajectories.

This shift has important theoretical implications. It suggests that the central question in behavioral finance may not be why investors behave differently, but how they become different. The former focuses on observable decisions, whereas the latter focuses on the processes that generate those decisions over time. By addressing this neglected dimension, the study extends behavioral finance beyond the explanation of behavioral anomalies toward a more comprehensive understanding of investor development.

Accordingly, the contribution of this study lies not only in identifying a new framework but also in redirecting attention toward identity formation as a fundamental mechanism underlying investment behavior. This perspective provides a foundation for future research seeking to connect psychological processes, learning experiences, and long-term behavioral outcomes within financial markets.

6. Conclusion

This study develops a substantive theory explaining how investor identities emerge through the interaction of financial knowledge and locus of control. Drawing on a constructivist grounded theory approach, the findings demonstrate that investor identity is not a fixed characteristic nor a direct consequence of demographic attributes or financial literacy alone. Instead, investor identity develops through an iterative process involving market exposure, knowledge acquisition, outcome interpretation, and behavioral adaptation.

The study contributes to behavioral finance by shifting attention from investment decisions to investor identity formation. While previous research has largely focused on identifying behavioral biases and classifying investor types, the present findings suggest that investor identities are better understood as emergent outcomes of ongoing learning and interpretive processes. Financial knowledge functions as a cognitive resource that supports decision-making and reflection, whereas locus of control shapes how investors interpret success and failure. Through repeated cycles of experience and adaptation, these processes gradually produce distinct investor identities.

Theoretically, the proposed Investor Identity Formation Framework (IIFF) extends existing behavioral finance literature by providing a process-oriented explanation for investor heterogeneity. Rather than asking why investors behave differently, the framework explains how they become different. This perspective offers a deeper understanding of the mechanisms underlying long-term investment behavior and identity development.

Practically, the findings suggest that investor education initiatives should move beyond the transmission of financial knowledge alone. Programs designed to improve investment behavior may also benefit from addressing how individuals interpret financial outcomes, develop self-efficacy, and construct their identities as investors.

Several limitations should be acknowledged. The study focuses on individual investors within a specific context and employs a qualitative design aimed at theory generation rather than statistical generalization. Future research may examine the applicability of the proposed framework across different investor populations and validate its relationships using quantitative or mixed-method approaches. Such efforts would further advance understanding of the developmental processes underlying investor identity formation.

7. Limitations

Several limitations should be considered when interpreting the findings of this study. First, the research employed a constructivist grounded theory approach aimed at generating theoretical explanations rather than producing statistically generalizable findings. Consequently, the proposed Investor Identity Formation Framework (IIFF) should be understood as a substantive theory grounded in participants' experiences rather than a universally applicable model.

Second, the study focused exclusively on individual investors with active investment experience. Although this focus was necessary to explore identity formation processes in depth, it may not fully capture the experiences of novice investors, institutional investors, or individuals operating in different financial contexts. Variations in market environments, investment cultures, and regulatory settings may influence how investor identities develop.

Third, the findings rely on retrospective accounts of participants' investment journeys. While such narratives provide valuable insights into identity construction, they may be influenced by recall bias and post hoc interpretations of past experiences. Investor identities are dynamic and may evolve over time, whereas the present study captures these processes at a particular stage of participants' investment careers.

Finally, although financial knowledge and locus of control emerged as central mechanisms in the identity formation process, other potentially relevant factors, including social influence, financial technology adoption, market sentiment, and personality characteristics, were beyond the scope of the current investigation. Incorporating these dimensions may provide a more comprehensive understanding of investor identity development.

8. Future Research Directions

The findings open several avenues for future research. First, quantitative studies may be conducted to examine the applicability of the Investor Identity Formation Framework (IIFF) across broader investor populations. Such studies could test the relationships among financial knowledge, locus of control, behavioral adaptation, and investor identity using survey-based or mixed-method designs.

Second, future research may investigate how investor identities evolve over time through longitudinal approaches. Because identity formation is inherently dynamic, longitudinal studies would provide deeper insights into how market experiences, economic cycles, and major financial events influence identity development across different stages of investors' careers.

Third, comparative studies across countries, cultures, and regulatory environments may reveal contextual factors that shape investor identity formation. As investing becomes increasingly globalized and technology-driven, understanding how identities emerge in different institutional settings represents an important area for future inquiry.

Finally, future research may extend the framework by incorporating additional psychological and social mechanisms, such as self-efficacy, social learning, financial influencers, online investment communities, and technological engagement. Examining these factors would contribute to a more comprehensive theory of investor identity formation and further advance behavioral finance research beyond traditional decision-making models.

Section

References

- Addo, J. O., Cúg, J., Keelson, S. A., Amoah, J., & Petráková, Z. (2025). Behavioral Risk Management in Investment Strategies: Analyzing Investor Psychology. International Journal of Financial Studies, 13(2). DOI ↗ Google Scholar ↗

- Ahmad, F. (2025). Personality-driven value investing: The mediating role of financial self-efficacy and versatile cognitive styles. Journal of Behavioral and Experimental Finance, 48(July), 101114. DOI ↗ Google Scholar ↗

- Almansour, B. Y., Elkrghli, S., & Almansour, A. Y. (2023). Behavioral finance factors and investment decisions: A mediating role of risk perception. Cogent Economics and Finance, 11(2). DOI ↗ Google Scholar ↗

- Ardhiani, M. C., & Panjaitan, Y. (2023). Analysis of Financial Knowledge, Financial Awareness, and Financial Attitude on Investment Decisions in the Capital Market by Indonesian Millennial Generation. Journal of Economics, Finance and Management Studies, 06(05), 2042–2049. DOI ↗ Google Scholar ↗

- Aristei, D., & Gallo, M. (2021). Financial knowledge, confidence, and sustainable financial behavior. Sustainability (Switzerland), 13(19). DOI ↗ Google Scholar ↗

- Chen, F., Lu, X., & Wang, W. (2022). Informal financial education and consumer financial capability: The mediating role of financial knowledge. Frontiers in Psychology, 13(November). DOI ↗ Google Scholar ↗

- Chen, W., Lu, B., Tian, J., & Ye, Y. (2026). Knowledge and asymmetric effects of investor sentiment on fund market resilience: Evidence from a large language model analysis. Journal of Innovation and Knowledge, 17(May), 101067. DOI ↗ Google Scholar ↗

- DOI ↗ Google Scholar ↗

- Cheng, Z. (2022). Psychology Analysis of Investors from the Perspective of Behavioral Finance. Atlantis Press International BV. DOI ↗ Google Scholar ↗

- Cho, S. W., & Jung, J. Y. (2024). Behavioral Finance Insights into Land Management: Decision Aggregation and Real Estate Market Dynamics in China. Land, 13(9). DOI ↗ Google Scholar ↗

- Corzo, T., Hernán, R., & Pedrosa, G. (2024). Behavioral finance in a hundred keywords. DOI ↗ Google Scholar ↗

- Heliyon, 10(16). DOI ↗ Google Scholar ↗

- Darwish, F. S. eed M. (2025). Financial literacy and investment decision: an empirical study from the Palestine Stock Exchange. Frontiers in Behavioral Economics, 4(2009). DOI ↗ Google Scholar ↗

- Gethe, R. K., Bajaj, A., & Hulage, M. S. (2022). Behavioural finance: understanding impact of human behaviour towards financial decision making. International Journal of Economics and Accounting, 11(2), 182. DOI ↗ Google Scholar ↗

- Grinblatt, M., & Keloharju, M. (2000). The investment behavior and performance of various investor types: A study of Finland’s unique data set. Journal of Financial Economics, 55(1), 43–67. DOI ↗ Google Scholar ↗

- Gunawan, H. (2024). The Pickle Jar Theory and Effective Time Management: A Philosophical Review. Technium Social Sciences Journal, 66, 287–298. DOI ↗ Google Scholar ↗

- Gupta, A., & Goswami, S. (2024). Behavioral perspective on sustainable finance: nudging investors toward SRI. Asian Journal of Economics and Banking, 8(3), 366–390. DOI ↗ Google Scholar ↗

- Jia, X. (2026). Investors’ Risk Aversion Preference from the Perspective of Behavioral Finance. Exploring Science Academic Conference Series, 10, 225–233. DOI ↗ Google Scholar ↗

- Koskelainen, T., Kalmi, P., Scornavacca, E., & Vartiainen, T. (2023). Financial literacy in the digital age—A research agenda. Journal of Consumer Affairs, 57(1), 507–528. DOI ↗ Google Scholar ↗

- Kumar, P., Islam, M. A., Pillai, R., & Sharif, T. (2023). Analysing the behavioural, psychological, and demographic determinants of financial decision making of household investors. Heliyon, 9(2), e13085. DOI ↗ Google Scholar ↗

- Kurniawati, R., Suparlinah, I., & Farida, Y. N. (2022). The effect of investment understanding, risk perception, income, and investment experience on investment behavior on capital market investors in Klaten District. Fair Value: Jurnal Ilmiah Akuntansi Dan Keuangan, 4(9), 3995–4004. DOI ↗ Google Scholar ↗

- Lusardi, A. (2019). Financial literacy and the need for financial education: evidence and implications. Swiss Journal of Economics and Statistics, 155(1), 1–8. DOI ↗ Google Scholar ↗

- Mahmood, F., Arshad, R., Khan, S., Afzal, A., & Bashir, M. (2024). Impact of behavioral biases on investment decisions and the moderation effect of financial literacy; an evidence of Pakistan. Acta Psychologica, 247(September 2023), 104303. DOI ↗ Google Scholar ↗

- DOI ↗ Google Scholar ↗

- Marjerison, R. K., Dong, H., & Kim, J. M. (2025). Generational Investment Behavior: The Influence of Risk Tolerance and Technology Adoption in an Evolving Financial Landscape. SAGE Open, 15(3), 1–20. DOI ↗ Google Scholar ↗

- Morris, T., Maillet, S., & Koffi, V. (2022). Financial knowledge, financial confidence and learning capacity on financial behavior: a Canadian study. Cogent Social Sciences, 8(1). DOI ↗ Google Scholar ↗

- Nogueira, M. C., Almeida, L., & Tavares, F. O. (2025). Financial Literacy, Financial Knowledge, and Financial Behaviors in OECD Countries. Journal of Risk and Financial Management, 18(3), 1–15. DOI ↗ Google Scholar ↗

- Padi, A., Musah, A., Blay, M. W., & Okyere, D. O. (2025). Small and Medium Scale Enterprise (SME) Owner financial literacy, entrepreneurial competencies and financial performance: the role of corporate governance. Future Business Journal, 11(1). DOI ↗ Google Scholar ↗

- Rao, H. P., Venkateswara, D., Bhanotu, R., Hari, B., & Rao, P. (2025). The fintech revolution: How digital trading platforms reshape retail investment. Journal of Marketing & Social Research, 2(6), 114–125. DOI ↗ Google Scholar ↗

- Rasa, K. (2024). Decision-Making : From Classical Finance To Behavioral. JOURNAL of BUSINESS ECONOMICS & MANAGEMENT, 25(5), 1–24. DOI ↗ Google Scholar ↗

- Rehman, K., & Mia, M. A. (2024). Determinants of financial literacy: a systematic review and future research directions. Future Business Journal, 10(1), 1–25. DOI ↗ Google Scholar ↗

- Shunmugasundaram, V., & Sinha, A. (2025). The impact of behavioral biases on investment decisions: a serial mediation analysis. Journal of Economics, Finance and Administrative Science, 30(59), 5–21. DOI ↗ Google Scholar ↗

- Sood, K., Pathak, P., & Singh, S. (2023). Behavioral finance and investor types: managing behavior to make better investment decisions. Qualitative Research in Financial Markets, 15(5), 907–912. DOI ↗ Google Scholar ↗

- Soumya, R., & Padmavathi, S. M. (2025). Financial literacy and Its influence on investment behaviour. International Journal of Social Impact, 10(2), 425–436. DOI ↗ Google Scholar ↗

- Wang, Y. (2026). Investor attention, investor sentiment and media in stock market: A literature review and research agenda. International Review of Economics and Finance, 106(July 2025), 104955. DOI ↗ Google Scholar ↗

- Yavuz, M. S., Tatlı, H. S., & Bozkurt, G. (2025). Exploring the financial impact of digital transformation: A comprehensive analysis on firms. Journal of Innovation and Knowledge, 10(5). DOI ↗ Google Scholar ↗

- Yusup, R., & Jasuni, A. Y. (2024). The Role of Financial Knowledge and Personality on Financial Management Behavior. Jurnal Manajemen Bisnis, 11(1), 340–351. DOI ↗ Google Scholar ↗

- Zapryanova, T., & Radeva, T. (2025). Theoretical Foundation of Locus of Control and its Influence in Working Environment. International Scientific Journal “Industry 4.0,” 10(6), 225–227. DOI ↗ Google Scholar ↗