Abstract

This study seeks to examine and clarify how Financial Literacy (FinLit) and financial behavior influence investment decision-making, with locus of control positioned as a mediating variable among young investors in Indonesia. The sample consisted of 240 young investors who use digital investment platforms such as Stockbit, RHB Securities, Bibit, and Ajaib. Data were gathered through an online questionnaire employing a Likert scale to assess each research variable, and the analysis was performed using Structural Equation Modeling (SEM) with AMOS. The descriptive results reveal that locus of control is positively and significantly affected by both FinLit and financial behavior. In addition, FinLit, financial behavior, and LoC each demonstrate a positive and significant impact on the investment decisions of young investors, underscoring the importance of cognitive, behavioral, and psychological aspects in shaping rational investment choices. Mediation testing further shows that locus of control partially mediates the relationships between FinLit, financial behavior, and investment decisions. Overall, these findings suggest that improving FinLit and encouraging sound financial behavior can enhance the quality of investment decisions, particularly when supported by a strong internal locus of control among young investors in Indonesia.

Keyword : FinLit, Financial Behavior, Locus of Control, Investment Decisions

Introduction

In recent years, the Indonesian capital market has shown a notably strong and encouraging upward trend. This growth is reflected in the substantial rise in the number of domestic investors participating in the market, supported by advancements in the digitalization of financial services across various sectors. Investment access has become increasingly available to the broader public, making investment activities more inclusive and efficient. Additionally, the capital market is playing an expanding role in promoting public participation in the formal financial sector. This trend demonstrates that investment has become a vital component of the economic behavior of modern society.

Data from the Indonesian Central Securities Depository (KSEI) reveals a rapid surge in the number of investors, growing from millions to tens of millions within a short period. This increase reflects a shift in people's financial management patterns, with capital market instruments increasingly viewed as attractive investment alternatives. The ease of opening securities accounts has significantly contributed to this accelerated growth, while digital platforms facilitate fast and convenient transactions. These trends indicate that Indonesia's investment ecosystem is evolving in a more advanced and sophisticated direction.

Behind this growth lies an intriguing demographic dynamic worth examining. Young investors still dominate in absolute numbers; however, their proportion of total investors is declining. This trend indicates challenges in sustaining consistent participation among the younger generation. Economic, psychological, and social factors may contribute to this decline. Young investors often face limited experience and income stability. Therefore, a thorough understanding of their characteristics is essential.

Young investors are known for their adaptability to technology and their eagerness to embrace financial innovations. They actively use digital investment applications, and high digital literacy is a crucial asset for participating in capital markets. This group also demonstrates early awareness of the importance of future investments. However, their investment decisions are influenced by various factors. Among these, FinLit and financial behavior are particularly significant. Additionally, psychological factors, such as LoC, play an important role.

In practice, young investors' investment decisions aren't always rational. Many decisions are Influenced by short-term trends on social media, community recommendations often serve as the primary basis for consideration. This situation can encourage speculative behavior. Their lack of experience makes them vulnerable to analytical errors, and financial planning discipline is often not yet firmly established. As a result, the risk of loss can increase within this group.

Initial observations suggest that young investors make generally sound investment decisions and typically have clear investment goals. However, there are notable weaknesses in their risk assessment practices. Additionally, consistency in adhering to personal investment policies is often lacking. Some investors remain uncertain about how to formulate long-term strategies. Variations in understanding among individuals highlight a competency gap, underscoring the need to strengthen the factors that support effective investment decision-making.

LoC is an important psychological factor that reflects an individual’s belief about what determines the outcomes in their life. People with a strong internal LoC tend to believe that success is largely shaped by their own efforts and decisions, leading them to assume greater responsibility for the choices they make. In investment contexts, this perspective encourages more careful evaluation and in-depth analysis before acting. In contrast, individuals with an external LoC are more likely to attribute results to outside forces such as luck, circumstances, or other people. These differing orientations play a significant role in influencing the quality of investment decisions.

FinLit has an important role in influencing LoC. A strong grasp of financial concepts helps build investor confidence in managing and directing their financial decisions, enabling individuals to believe that their personal decisions influence outcomes. Additionally, FinLit aids in assessing investment risks and opportunities. Educated investors tend to be more systematic in planning strategies and are less susceptible to misleading information. Therefore, FinLit strengthens an internal locus of control orientation.

Although young investors generally possess a good level of FinLit, certain weaknesses persist. Understanding the relationship between risk and return is not yet widespread. Some investors struggle to comprehensively evaluate investment instruments. Furthermore, their financial behaviors are often less than ideal. Monthly spending plans are not consistently followed, and saving habits as well as preparations for financial protection remain limited. This condition may adversely influence the quality of the investment decisions they make.

Considering this phenomenon, the study becomes increasingly relevant. It aims to examine how FinLit and financial behavior influence investment decision-making, with locus of control (LoC) acting as a mediating variable that connects these factors. The research focuses on young investors in Indonesia as its primary target group. The findings are expected to offer a comprehensive empirical perspective that can be used as a basis for designing more effective financial education strategies. Ultimately, this effort aims to sustainably enhance the quality of investment decisions made by the younger generation.

Literature Review

Investment Decisions

Investment decisions are a crucial aspect of financial behavior, especially for young investors building their financial foundations. According to [1], investment decisions involve the financial management process of selecting and evaluating long-term projects or assets expected to generate future cash flows, with the goal of increasing both the company's value and the investor's wealth. In an individual context, investment decisions are understood as strategies for allocating funds to specific financial instruments or assets with the expectation of profit, either through direct management or asset appreciation [2]

nvestment decisions involve determining how to allocate funds across various assets or projects expected to yield future benefits, taking into account associated risks and anticipated rates of return [3]. Meanwhile [4] define investment decisions as those related to capital expenditures (capital budgeting), specifically how companies plan and manage investments in projects or assets expected to generate added value over the medium and long term. Young investors tend to face different dynamics compared to mature investors. They have a longer investment horizon but often lack experience and possess limited financial knowledge [5]. These factors influence how they make investment decisions.

Therefore, it can be inferred that the investment decisions of young investors are strongly shaped by a range of both internal and external factors. Internal factors include financial knowledge, experience, and attitudes toward risk, while external factors encompass market conditions, regulations, and access to information. This study highlights that investment decisions should not be assessed only from the standpoint of economic rationality, but also from a behavioral perspective, particularly for young investors who are still in the initial phase of developing their financial experience and decision-making skills. In this research, investment decisions are measured using indicators outlined by [2] namely: (1) Rate of return, (2) time factor, (3) risk, (4) investment objectives, (5) determination of investment policy.

Locus of Control

LoC refers to an individual’s general inclination to perceive the outcomes of events as either the result of their own actions and efforts (internal) or as being influenced by external elements such as luck, fate, or other outside forces [6]. Additionally, [7] describe LoC as a psychological construct that reflects the degree to which a person believes that success or failure in life is determined by their own actions and efforts or by external factors that are beyond their control.

[8] defines LoC as an individual's preference for agency that is, the ability to control outcomes rather than dependence on others or external conditions when making economic decisions. Meanwhile, [9], the originator of this concept, states that LoC reflects the degree to which individuals believe that the outcomes or reinforcements they experience are the result of their own actions and personal attributes (internal), rather than being shaped by external forces such as luck, fate, or the influence of others (external).

[10] expanded on Rotter's view by stating that LoC is not only divided into internal and external categories but can also be further subdivided. For example, external factors can originate from chance or from the influence of others (powerful others). This distinction enriches the understanding of the dimensions of LoC. Furthermore, [11], emphasized the application of LoC in the work context by defining it as the degree to which individuals perceive that events in the workplace are determined by their own control or shaped by external factors beyond their influence.

Based on the development of definitions and research findings, LoC can be understood not merely as a psychological construct distinguishing internal from external orientations, but rather as a multidimensional spectrum that is both contextual and dynamic. In the modern context, LoC is influenced by personal factors (such as literacy and self-efficacy), social factors (including support from others and group norms), and structural factors (such as access to information, regulations, and technology). This demonstrates that LoC is not static; it can change and is shaped by experience, learning, and the environment. LoC is not only a personality trait but also an adaptive mechanism that plays a crucial role in determining individual behavior, including investment decisions, financial management, and performance achievement in daily life.

In this research, the LoC was measured using indicators outlined by [10] and [11], namely: 1. Internal LoC, characterized by personal responsibility, effort and hard work determining results, initiative and proactiveness, planning and self-control, and confidence in personal abilities; 2. External LoC, characterized by belief in fate or luck, influence by authorities, an external environment that is difficult to control, lack of motivation to try, and the perception that personal effort does not always correlate with success. Reason: Corrected punctuation and spacing around citations, clarified terminology by spelling out

FinLit

According to Financial Services Authority Regulation No. 76/POJK.07/2016, financial literacy emphasizes the role of individual knowledge and skills in determining the direction of personal financial policies for better well-being. Similarly, [12] broadens this scope by including an in-depth understanding of the dynamics of financial products. This encompasses the ability to optimally operate financial services while protecting oneself from potential losses.

The ability to process financial information rationally depends heavily on an individual's level of financial literacy. [13] views it as a synergy between attitudes, understanding, and actions that is crucial for effective decision-making and financial risk mitigation. On the other hand, [14] emphasizes mastery of basic materials such as savings and risk management, where this understanding is key for individuals to act optimally in facing economic dynamics.

Financial literacy is now a crucial element amidst the increasingly complex diversity of financial products. Individuals with a strong financial understanding tend to be more adept at designing future strategies, managing potential risks, and selecting the most appropriate investment instruments [2]; [12]. This phenomenon impacts not only individuals but also at a macro scale; as stated by [13], the involvement of a financially savvy society is a catalyst for the creation of an inclusive financial system and strengthening a country's economy.

With the diversification of financial instruments, mastering financial literacy is no longer merely an option, but a necessity. This is because financial literacy not only impacts the effectiveness of personal financial management but also serves as a supporting pillar for macroeconomic resilience. Therefore, the urgency of this research lies in analyzing the behavior of young investors in determining their financial steps. To measure this level of literacy, this research refers to four main dimensions according to [12]: (1) basic financial knowledge, (2) personal financial management, (3) investment and risk, (4) financial planning.

Financial Behavior

[15] state that financial behavior encompasses a series of actions individuals take to effectively manage their financial resources. This includes the processes of planning, monitoring, and allocating financial resources to meet both short-term and long-term financial objectives. Such behavior involves activities like preparing a budget, managing debt, saving funds, investing, and securing financial protection through insurance.

Financial behavior refers to how individuals manage their income and overall financial situation, reflecting their approach to everyday financial matters. It demonstrates a person’s ability to handle finances effectively to achieve life goals and financial success. [16] explain that financial behavior encompasses how individuals decide to use their money, including routine financial decisions that contribute to a sense of financial security.

Based on these definitions, financial behavior is a key component of personal finance studies, as it relates to how individuals manage their financial resources, including spending patterns, saving habits, investment decisions, and debt management. It not only reflects a person’s actions in handling money but also encompasses the attitudes, habits, and decision-making processes that guide the use of financial resources.

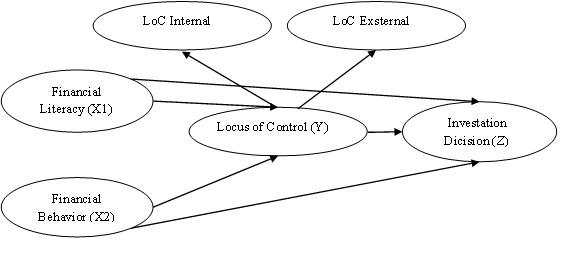

Framework

Research methods

This research was conducted in Indonesia, focusing on young investors aged 15 to 30 years who actively invest through the capital market and other financial instruments via digital investment platforms such as Stocbit, RHB Securities, Bibit, and Ajaib. The study examines FinLit, financial behavior, locus of control, and investment decisions. To determine the sample size, this study follows the guidelines proposed by [17], which recommend that the number of respondents should be 5 to 10 times the total number of research indicators. Since this study employs 24 indicators, the minimum required sample size is 240 respondents (10 × 24 = 240). This sample size ensures that the data obtained are sufficiently robust and reliable for SEM analysis.

With an adequate number of respondents, the study is expected to yield more precise conclusions about the relationships among the variables examined. Data were collected using an online questionnaire distributed via the following link: https://bit.ly/T-Eri-Firtana. The questionnaire was shared through WhatsApp groups for members of the investment platform. Responses were measured using a 5-point Likert scale (STS, TS, KS, S, SS) because the Likert scale effectively captures respondents' perceptions of the variables being studied.

Results and Discussion

Descriptive

The results of the descriptive testing are as shown in Table 1 below:

| Test Value = 3.41 | |||||||

| Rerata | t | df | Sig. (2-tailed) | Mean Difference | 95% Confidence Interval of the Difference | ||

| Lower | Upper | ||||||

| Invesment Dicisions | 3.86 | 139.865 | 238 | .000 | 15.88707 | 15.6633 | 16.1108 |

| Locus of Control | 3.36 | 96.691 | 238 | .000 | 21.95820 | 21.5108 | 22.4056 |

| FinLit | 3.68 | 75.800 | 238 | .000 | 11.29711 | 11.0035 | 11.5907 |

| Financial Behavior | 3.84 | 86.630 | 238 | .000 | 15.79502 | 15.4358 | 16.1542 |

Statistically, a two-tailed significance value of less than 0.05 indicates that the research dimensions are effective among young investors in Indonesia. This consistent data provides a strong basis for accepting Ha1 and rejecting Ho1. Therefore, the first hypothesis in this study has been empirically tested and confirmed.

Direct Effect

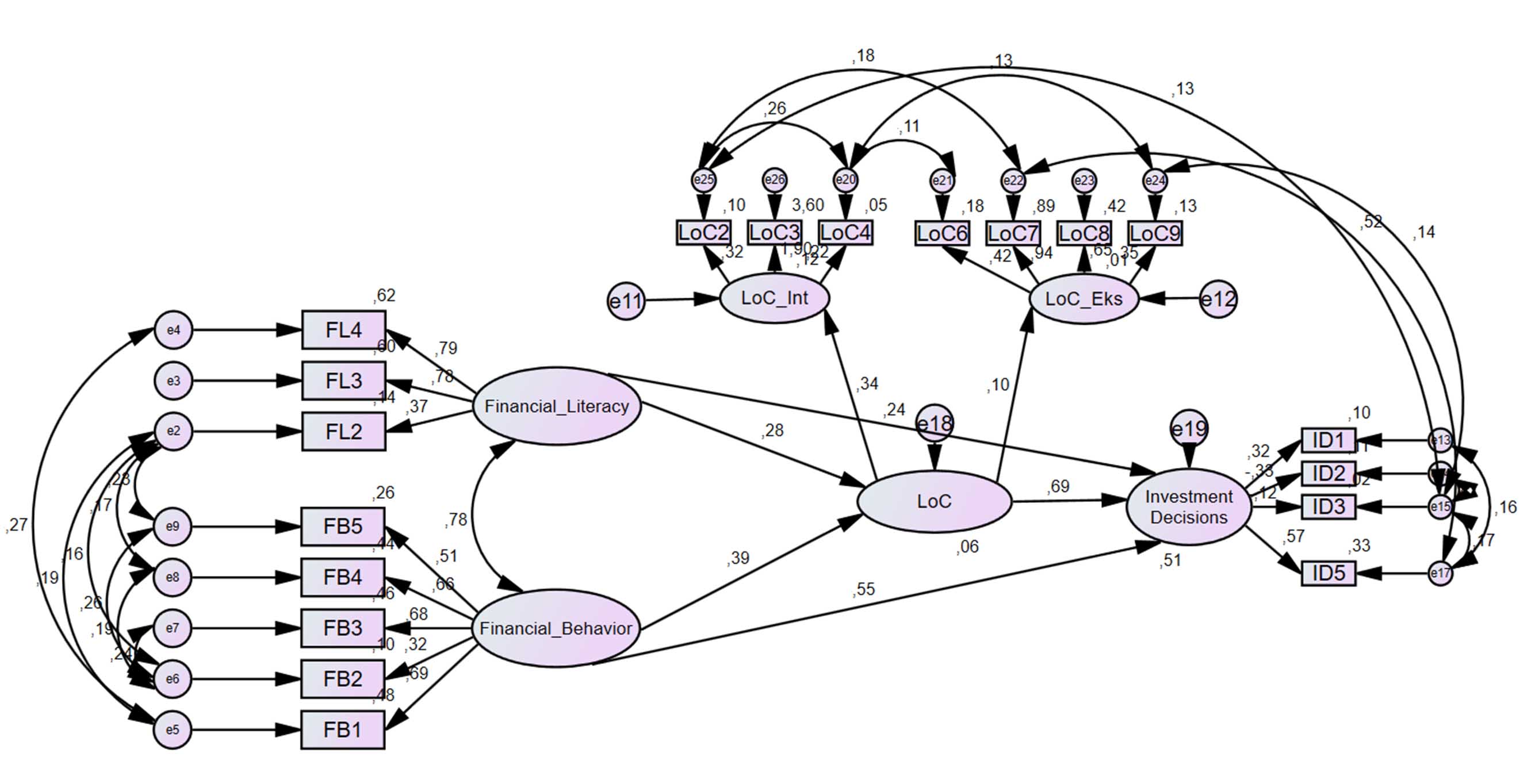

The results of the direct hypothesis are as shown in Figure 2 below

A comprehensive model test produced analytical results concerning the direct hypotheses, as shown in the table below.

| Endogen | Eksogen | Estimate | S.E. | C.R. | P | ||

| Ustd | Std | ||||||

| LoC | <--- | Financial_Literacy | .271 | .284 | .088 | 2.803 | *** |

| LoC | <--- | Financial_Behavior | .341 | .393 | .046 | 2.891 | *** |

| Investment_Decisions | <--- | LoC | .594 | .694 | .081 | 2.583 | *** |

| Investment_Decisions | <--- | Financial_Literacy | .186 | .240 | .110 | 4.783 | *** |

| Investment_Decisions | <--- | Financial_Behavior | .483 | .551 | .056 | 3.479 | *** |

H2: The Influence of FinLit on Locus of Control

The results of the direct analysis indicate that FinLit has a positive and statistically significant effect on the LoC of young investors in Indonesia. This is demonstrated by a CR value of 2.803, which exceeds the threshold of 1.96, and P: 0.000, which is below the 5% significance level. These findings suggest that higher levels of FinLit enhance the locus of control among young investors. The standardized estimate of 0.284, or 28.4%, indicates that FinLit substantially contributes to shaping individuals' beliefs about their control over decisions and the financial outcomes they achieve.

The findings of this study align with previous research indicating a positive association between FinLit and locus of control (LoC). Studies by [18] and [19] demonstrate that individuals with higher levels of FinLit tend to exhibit greater self-confidence, increased independence, and a stronger sense of control over their financial decision-making.

FinLit also enhances young investors' confidence in the effectiveness of financial planning [19]. Individuals who understand the importance of financial planning can set clear investment goals, develop measurable strategies, and evaluate their decisions effectively. This knowledge helps young investors avoid overreliance on external factors such as market fluctuations, others' opinions, or luck. Therefore, FinLit serves not only as a source of knowledge but also as a psychological factor that fosters a stronger internal LoC, promoting independence and responsibility in investment decision-making.

The research results indicate that increasing LoC in young investors can be achieved by enhancing FinLit in four key areas. First, understanding basic financial concepts such as income, expenses, inflation, interest, and the time value of money provides a foundation for recognizing the impact of financial decisions on the future. Second, improving personal financial management skills through budgeting, tracking cash flow, and controlling expenses helps individuals understand the relationship between financial discipline and outcomes. Third, deepening knowledge about investments and risk including the characteristics of financial instruments, the risk-return relationship, and strategies like diversification encourages rational and responsible decision-making. Finally, strengthening long-term financial planning by setting clear goals and implementing targeted savings and investment strategies increases individuals’ confidence that their future financial well-being is within their control.

H3: The Influence of Financial Behavior on Locus of Control

The analysis indicates that financial behavior has a positive and statistically significant influence on the locus of control (LoC) of young investors in Indonesia. This is demonstrated by a C.R: 2.891 and P: 0.000. confirming the significance of the relationship. These findings suggest that financial behavior plays a crucial role in enhancing young investors’ confidence in their ability to manage financial decisions and outcomes. The effect size (E.S.) of 0.393 indicates that financial behavior strongly contributes to LoC, implying that improving financial behavior can increase LoC among young investors in Indonesia by 39.3%. These results are consistent with studies conducted by [20] and [21].

Investors who exhibit sound financial behavior tend to proactively seek continuous learning about financial management, comprehend the consequences of each financial decision, and independently assess the outcomes achieved [20]. A strong belief in the effectiveness of financial planning leads young investors to perceive financial success or failure as the result of their own actions and decisions, rather than being solely influenced by external factors such as market fluctuations, environmental pressures, or advice from others [20]. This mindset reinforces an internal LoC orientation and motivates young investors to become more independent and responsible in managing their finances [21].

The research concludes that improving the LoC in young investors through financial behavior can be achieved by implementing systematic and realistic financial planning, controlling expenses through budgeting and disciplined differentiation between needs and wants, managing debt wisely according to one’s capacity, developing the habit of saving and investing regularly based on goals and risk profiles, and preparing financial protections such as emergency funds or insurance. This planned, consistent, and self-disciplined financial behavior not only significantly enhances financial conditions but also strengthens a sense of responsibility, independence, and confidence that one’s financial future is within their control.

H4:The Influence of FinLit on Investment Decisions

The direct testing results for H4 indicate that FinLit has a positive and statistically significant impact on the investment decisions of young investors in Indonesia. This is evidenced by a C.R: 4.783, and P: 0.000, confirming the significance of the relationship. The E.S. value of 0.240 suggests that FinLit accounts for 24% of the variance in the quality of investment decisions made by young investors. Therefore, higher levels of FinLit encourage young investors to make more rational, well-planned investment decisions based on a better understanding of financial information.

Based on the respondents' answers to the questionnaire, it was evident that some young investors still lack the understanding and readiness to make optimal investment decisions. This finding highlights a gap between their financial knowledge and its practical application in investment decision-making. Therefore, efforts to improve investment decisions should focus on enhancing applied FinLit, enabling young investors not only to grasp financial concepts theoretically but also to apply them effectively in real-life investment situations [22], [12]. Improved FinLit is expected to reduce young investors' reliance on external influences such as recommendations from others, temporary trends, and emotions, thereby promoting more independent and objective decision-making.

Improving the investment quality of young investors through FinLit involves strengthening foundational knowledge, including inflation, interest rates, the time value of money, and the relationship between risk and return, which serve as the basis for assessing investment feasibility. It also entails enhancing personal financial management skills through budgeting, cash flow control, and proportional allocation of investment funds. Additionally, it requires deepening understanding of various investment instruments, their risk characteristics, and strategies such as diversification to enable more rational and prudent decision-making. Finally, developing clear long-term financial plans to establish investment goals, strategies, and ongoing evaluations helps ensure that investment decisions become more mature, independent, and responsible.

H5: The Influence of Financial Behavior on Investment Decisions

The direct testing results for Hypothesis 5 demonstrate that financial behavior has a positive and statistically significant effect on the investment decisions of young investors in Indonesia. This is evidenced by a C.R: 3.479, which exceeds the threshold at the 5% significance level, and a p-value of 0.000, confirming the strength of the relationship. The E.S. value of 0.551 indicates that financial behavior accounts for 55.1% of the improvement in the quality of investment decisions among young investors. These findings are consistent with previous studies conducted by [22], [23]. Overall, these results confirm that how individuals manage their daily finances plays a more dominant role than mere conceptual understanding in influencing investment decisions.

Although financial behavior has been shown to have a strong influence, respondents' answers indicate that some young investors are still not fully consistent in practicing healthy financial habits, resulting in suboptimal investment decisions. This suggests that the main challenge lies not only in the availability of information but also in the ability to translate knowledge into concrete actions [23]. Therefore, improving the quality of investment decisions among young investors should focus on developing sustainable financial habits and discipline, enabling decision-making to become more rational, deliberate, and less influenced by emotional factors or external pressures.

Improving the quality of investments for young investors through sound financial behavior can be achieved by developing a clear and realistic financial plan to guide the allocation of investment funds; controlling expenses to ensure the availability of sustainable investment capital; managing debt prudently according to one’s financial capacity to reduce stress; cultivating the habit of saving and investing regularly to build consistency and a long-term perspective; and establishing financial protection, such as emergency funds and insurance, to mitigate unexpected risks. These practices help ensure that investment decisions are made calmly, thoughtfully, and are supported by stable financial conditions and a disciplined, independent, and responsible mindset.

H6: The Influence of Locus of Control on Investment Decisions

The H6 test results indicate that LoC has a positive and statistically significant influence on the investment decisions of young investors in Indonesia. This is evidenced by a critical ratio (C.R.) of 2.583, which exceeds the critical threshold, and P: 0.000, confirming the statistical significance of the relationship. The E.S. value of 0.694 suggests that LoC accounts for 69.4% of the variance in investment decisions. These findings imply that an individual’s belief in their ability to control outcomes is a dominant factor in determining the quality of investment decisions made by young investors. The results are consistent with studies by [20], which also demonstrated that LoC plays a significant role in enhancing investment decisions.

Respondent responses indicate that some young investors are still not fully prepared or confident in making optimal investment decisions. This reflects a less than fully internal locus of control (LoC) orientation, which can cause young investors to be hesitant, easily influenced by their environment, and dependent on external factors such as fate, recommendations from authorities, or market conditions [9]. Therefore, improving the quality of investment decisions should focus on strengthening the internal LoC, enabling young investors to be more confident that investment success or failure results from personal responsibility, effort, and decision-making , [24].

Improving the quality of young investors' investment decisions by strengthening their internal LoC involves fostering a sense of responsibility for each decision, encouraging an objective evaluation of outcomes as learning opportunities, and reinforcing the belief that personal effort and ability determine results through increased analysis and consistency. It also requires taking the initiative to seek information independently rather than relying on others, and practicing planning and self-control through disciplined and measured investment strategies. Conversely, external LoC orientations such as dependence on fate, authority, or environmental conditions should be minimized by framing external factors as risks that can be anticipated. This approach helps young investors become more rational, independent, and long-term oriented in their investment decisions.

Indirect Effect

H7: The Influence of FinLit on Investment Decisions Through Locus of Control

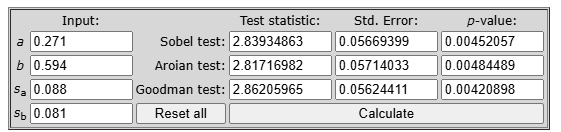

The results of validation of hypothesis 7 using the Sobel calculator are shown in Figure 3 below.

The analysis indicates that locus of control (LoC) partially mediates the relationship between FinLit and the investment decisions of young investors in Indonesia. This is supported by a t-statistic value of 2.839 and a P-value of 0.004, confirming the significance of the mediating effect. These results suggest that FinLit not only has a direct impact on investment decisions but also exerts an indirect influence through the development of LoC. In this context, LoC functions as a psychological mechanism linking FinLit to the quality of investment decisions made. Furthermore, the significance testing of path C' demonstrates that LoC plays a crucial role in mediating the effect of FinLit on investment decisions, as illustrated in the following figure.

Figure 4. Diagram of the Mediation Effect of Hypothesis 7

This partial mediation effect indicates that LoC accounts for 16% of the strengthening in the relationship between FinLit and investment decisions. This suggests that a stronger LoC among young investors can enhance the impact of FinLit on their investment decisions by 16%. Young investors with higher levels of FinLit are more likely to develop a strong internal LoC, which makes them more confident, independent, and consistent when making investment choices. However, because the mediation is partial, FinLit still directly influences investment decisions without relying entirely on LoC. These findings highlight that improving the quality of young investors’ investment decisions requires simultaneous efforts to strengthen FinLit and foster a more dominant internal LoC.

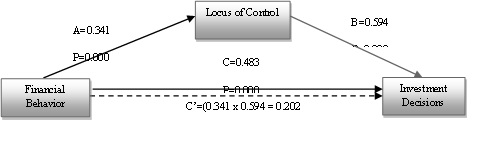

H8: The Influence of Financial Behavior on Investment Decisions Through Locus of Control

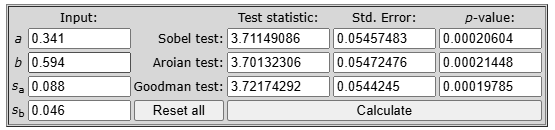

Figure 5 shows the results of testing hypothesis 8 analyzed using the Sobel calculator.

The Sobel test data indicate that the significance criteria have been met, with a value of t = 3.711 and p = 0.000; therefore, Hypothesis 8 is accepted. This finding suggests that financial behavior not only directly influences investment decisions but also indirectly affects them through the formation of the LoC as a psychological factor that strengthens this relationship. The calculation results for path C' are presented below.

The figure shows that the partial mediation effect indicates that the LoC contributes 20.2% to enhancing the influence of financial behavior on investment decisions. This value suggests that the impact of financial behavior on the quality of investment decisions operates by increasing an individual's belief in self-control over financial outcomes. Young investors who practice good financial behavior tend to have a stronger internal LoC, resulting in greater confidence, discipline, and independence when making investment decisions. However, due to the partial mediation effect, financial behavior still directly influences investment decisions without fully relying on the LoC. This finding confirms that efforts to improve investment decisions among young investors should focus on strengthening healthy financial behavior while simultaneously fostering a sustainable internal LoC.

Conclusion

The research findings on young investors in Indonesia who use the online platforms Stocbit, RHB Securities, Bibit, and Ajaib can be summarized as follows:

References

- Brigham Eugene F., Houston Joel F. Fundamentals of Financial Management Cengage Learning Boston 2021 DOI ↗ Google Scholar ↗

- Pozo Raquel González Measurement Scales on Investment Decision-making. Empirical Evidence Based on MiFID Questionnaires Behanomics 2 DOI ↗ Google Scholar ↗

- Gitman Lawrence J, Juchau Roger, Flanagan Jack Principles of Managerial Finance Pearson Higher Education AU Australia 2019 DOI ↗ Google Scholar ↗

- Ross Stephen A., Westerfield Randolph, Jaffe Jeffrey F. Corporate Finance McGraw-Hill/Irwin United Kingdom 2018 DOI ↗ Google Scholar ↗

- Nareswari Ninditya, Balqista Alifia Salsabila, Negoro Nugroho Priyo The Impact of Behavioral Aspects on Investment Decision Making Jurnal Manajemen dan Keuangan 10(1) DOI ↗ Google Scholar ↗

- Nowicki Stephen, Iles-Caven Yasmin, Kalechstein Ari, Golding Jean Editorial: Locus of Control: Antecedents, Consequences and Interventions Using Rotter's Definition Frontiers in Psychology 12 DOI ↗ Google Scholar ↗

- Papoulidi Asimenia, Maniadaki Katerina The Mediating Role of Self-Efficacy in the Relationship Between Locus of Control and Resilience in Primary School Students European Journal of Investigation in Health, Psychology and Education 15(7) DOI ↗ Google Scholar ↗

- Caliendo Marco, Cobb-Clark Deborah A., Silva-Goncalves Juliana, Uhlendorff Arne Locus of control and the preference for agency European Economic Review 165 DOI ↗ Google Scholar ↗

- Rotter Julian B. Generalized expectancies for internal versus external control of reinforcement Psychological Monographs: General and Applied 80(1) DOI ↗ Google Scholar ↗

- Levenson Hanna Multidimensional Locus of Control in Adults: A Preliminary Report Journal of Consulting and Clinical Psychology 41(3) DOI ↗ Google Scholar ↗

- Spector Paul E. Development of the Work Locus of Control Scale Journal of Occupational Psychology 61(4) DOI ↗ Google Scholar ↗

- Lusardi Annamaria, Mitchell livia S. The Economic Importance of Financial Literacy: Theory and Evidence Journal of Economic Literature 52(1) DOI ↗ Google Scholar ↗

- OECD OECD/INFE 2023 International Survey of Adult Financial Literacy OECD Publishing Paris DOI ↗ Google Scholar ↗

- Mitchell Olivia, Lusardi Annamaria Financial Literacy and Retirement Planning in the United States Journal of Pension Economics and Finance 10(4) DOI ↗ Google Scholar ↗

- Xiao Jing Jian, Dew Jeffrey The Financial Management Behavior Scale: Development and Validation Journal of Financial Counseling and Planning 22(1) 2011 DOI ↗ Google Scholar ↗

- Sabri Mohamad Fazli, Anthony Mervin, Law Siong Hook, Rahim Husniyah Abdul, Burhan Nik Ahmad Sufian, Ithnin Muslimah Impact of financial behaviour on financial well-being: evidence among young adults in Malaysia Journal of Financial Services Marketing 22 DOI ↗ Google Scholar ↗

- Sugiyono Metode Penelitian Bisnis Alfabeta Bandung 2017 DOI ↗ Google Scholar ↗

- Nisak Husnun, Musnadi Said, Sakir A. The Role of Locus of Control in Mediating the Influence of Financial Literacy, Financial Attitudes, and Lifestyle on the Personal Financial Management Behavior of Generation Z in Banda Aceh City International Journal of Scientific Research and Management 13(10) DOI ↗ Google Scholar ↗

- Khadijah Sitti, Fajriah Yana, Heslina Peran Locus of Control Sebagai Variabel Intervening: Pengaruh Literasi Keuangan dan Persepsi Risiko Terhadap Keputusan Investasi Management Studies and Entrepreneurship Journal 5(2) DOI ↗ Google Scholar ↗

- Bucciol Alessandro, Trucchi Serena Locus of control and saving: The role of saving motives Journal of Economic Psychology 86 DOI ↗ Google Scholar ↗

- Salamanca Nicolás, Grip Andries, Fouarge Didier, Montizaan Raymond Locus of control and investment in risky assets Journal of Economic Behavior & Organization 177 DOI ↗ Google Scholar ↗

- Putri Resiahati, Maivalinda Pengaruh Literasi Keuangan, Perilaku Keuangan, dan Persepsi Risiko terhadap Pengambilan Keputusan Investasi Mahasiswa Journal of Business Economics and Management 1(3) 2025 DOI ↗ Google Scholar ↗

- Parmitasari Rika Dwi Ayu, Syariati Alim, Sumarlin Chain Reaction of Behavioral Bias and Risky Investment Decision in Indonesian Nascent Investors Risks 10(8) DOI ↗ Google Scholar ↗

- Rahmawati Alni, Wahyuningsih Sri Handari, Garad Askar The effect of financial literacy, training and locus of control on creative economic business performance Social Sciences & Humanities Open 8(1) DOI ↗ Google Scholar ↗